Research Capital analyst Andre Uddin keeps “Speculative Buy” rating on Sernova Biotherapeutics

Research Capital analyst Andre Uddin maintained a “Speculative Buy” rating and C$0.60 price target on Sernova Biotherapeutics (Sernova Biotherapeutics Stock Quote, Chart, News, Analysts, Financials TSXV:SVA) in a June 16 report, citing strong early clinical results and a promising pipeline, but warning the company will need to secure more funding in the near term.

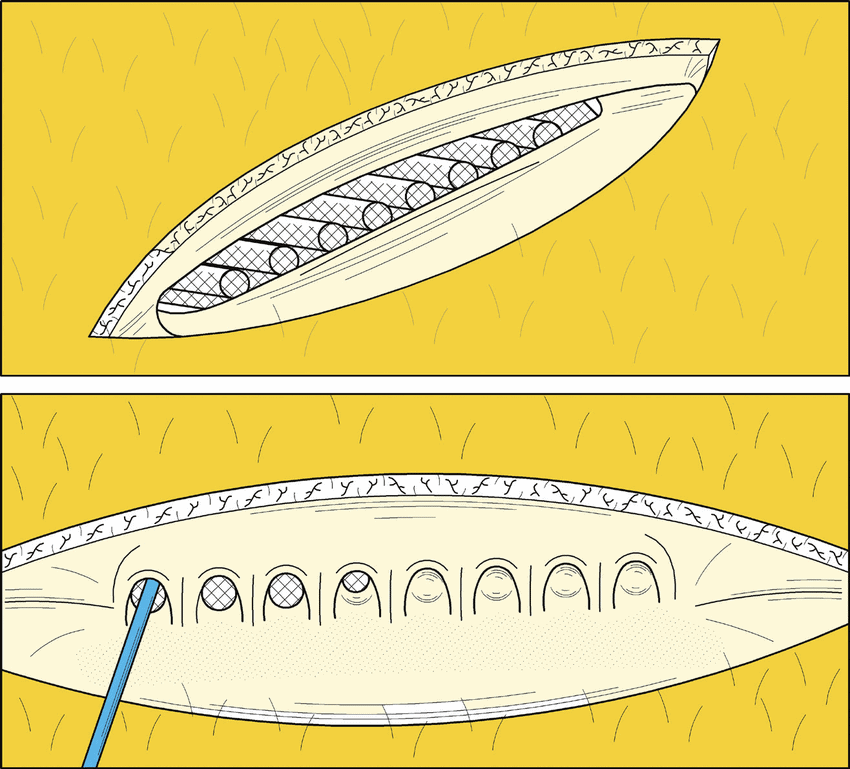

Sernova is a clinical-stage biotechnology company developing a cell therapy platform designed to treat chronic diseases, including type 1 diabetes, hypothyroidism, and hemophilia A.

Uddin said Sernova reported its Q2 results, though financials remain secondary as the company is still in the clinical stage. As of quarter-end, Sernova had $2-million in cash and $4.2-million in debt. During the quarter, it raised $1-million through a convertible debenture with board member Dr. Steven Sangha, and $4-million from Navigate Private Yield Fund LP III, managed by Fraser Mackenzie Private Credit Inc. The $4-million loan is secured against Sernova’s assets, its U.S. subsidiary, and Dr. Sangha. In connection with the loan, Sernova issued Sangha 9-million common share purchase warrants, exercisable at $0.20 for 36 months and subject to a four-month hold. The loan matures April 16, 2026, with fixed interest of $400,000 for the first six months, and 14.25% annually thereafter.

“While the recent debt financing rounds extend SVA’s cash runway through approximately Q4, 2025, we continue to believe that the company will need to secure additional funding in the near term,” Uddin said. “SVA is currently exploring financing opportunities with GoldTrack Ventures and the Kingdom of Saudi Arabia, which could represent potential sources of capital. The company has a compelling product that is well-positioned in the T1D clinical development landscape – if positive data emerges from the upcoming Cohort C of the ongoing Ph1/2 trial, which we believe is likely based on existing data, it could represent a meaningful value inflection point.”

Uddin said Sernova’s Q2 results reflect its status as a clinical-stage biotech, with earnings remaining secondary. Revenue was $0.0-million, in line with expectations and unchanged from last year. The net loss was $3.8-million, or $0.01 per share, better than the estimated $5.3-million loss, and an improvement from $9.9-million or $0.03 per share a year ago. As of quarter-end, Sernova had $2-million in cash and $4.2-million in debt.

Sernova shared encouraging early results from its ongoing Phase 1/2 trial for type 1 diabetes. In the study’s two patient groups, 8 out of 12 people no longer needed insulin shots, and 7 still showed healthy islet cell activity, based on key lab results. Other test scores and tissue samples confirmed that the transplanted cells were working. When it came to blood sugar control, 9 out of 12 patients had A1C levels below the recommended target of 7.0%. Of the other three, one improved from 10.3% to 7.8%, and the remaining two were already under 7% at the start and stayed there.

“We believe the trial is on track to meet its primary and secondary endpoints,” Uddin said. “We continue to await data from Cohort C (10-pouch; optimized immunosuppression), which is expected to begin enrolling patients by year-end 2025.”

-30-

Rod Weatherbie

Writer

Rod Weatherbie is a journalist based in Prince Edward Island. Since 2004, he has written extensively about the Canadian property and casualty insurance landscape. He was also a founder and contributing editor for a Toronto-based arts website and a PEI-based food magazine. His fiction and poetry have been featured in The Fiddlehead, The Antigonish Review, and Juniper.

Related Posts

Its most recent quarterly results are in the books, but Research Capital analyst Andre Uddin is looking in another place...

SERNOVA Following the release of new data on a core offering, Research Capital analyst Andre Uddin remains upbeat about the...