Is it time to sell your Byrna Technologies stock?

Roth Capital Partners analyst Matt Koranda says Byrna Technologies’ (Byrna Technologies Stock Quote, Chart, News, Analysts, Financials NASDAQ:BYRN) shift toward a broader self-defence market could take several quarters to show results.

In a July 10 update, Koranda downgraded Byrna to “Neutral” from “Buy” and lowered his target to $4.50 from $12.50.

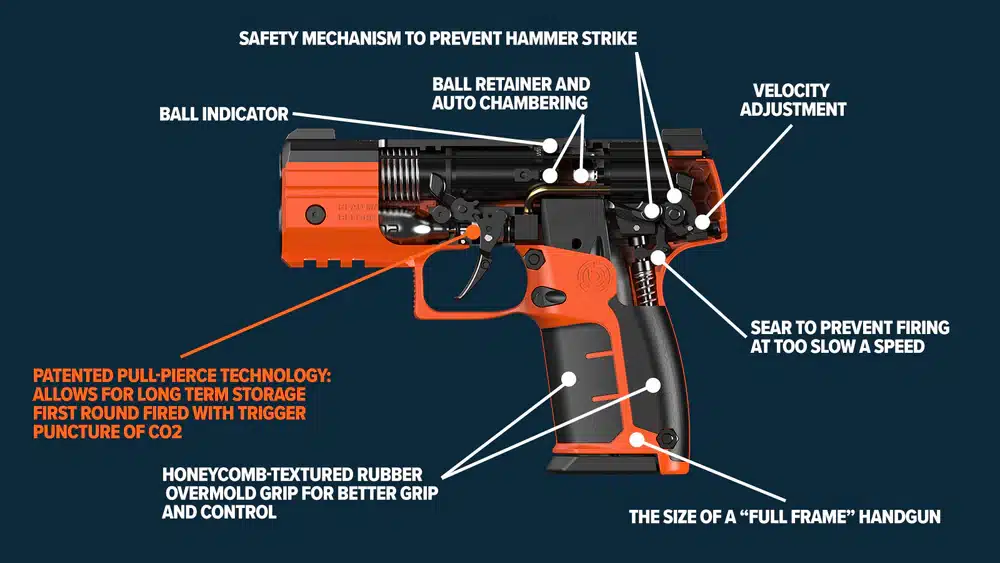

Byrna develops and sells less-lethal personal security products in the U.S., South Africa, Europe, South America, Asia and Canada. The company is headquartered in Andover, Mass.

“While shares already reflect much of the recent weakness, we believe meaningful fundamental improvement will take several quarters given the company’s strategic shift,” Koranda said.

The analyst said new CEO Conn Davis is trying to broaden Byrna’s appeal beyond its core customer base of mostly middle-aged firearms enthusiasts reached through politically conservative media channels.

Koranda said the strategy makes sense because less-lethal products could appeal to non-firearm households. But he said Byrna’s marketing, product mix and profitability have largely been built around a firearms-friendly customer base.

He said the transition could take time and require significant marketing and operating spending, particularly because lower-average-order-value less-lethal products are harder to sell profitably online.

“We’d like to see evidence that Byrna is acquiring new customers at attractive unit economics,” Koranda said. “This should show up in the form of a return to sales growth in the Direct channel, along with positive/growing EBITDA margin flow-through.”

Byrna reported Q2 sales of $16.4-million, down 43% year-over-year. Wholesale revenue fell 47% to $5.7-million after limited restocking orders, while direct revenue declined 35% to $11.0-million on lower traffic and conversion.

Adjusted EBITDA was negative $600,000, compared with positive results a year earlier, as lower sales and higher marketing spending pressured margins.

Management said Q3 sales trends are tracking in line with Q2, with a seasonal pickup expected in Q4. Gross margin is expected to remain around 62%, while continued marketing spending could keep Adjusted EBITDA negative in Q3.

Koranda lowered his fiscal 2026 forecast to revenue of $88.7-million and negative Adjusted EBITDA of $1.4-million from $118-million and positive Adjusted EBITDA of $8.6-million.

Byrna also announced a $1.25-million acquisition of HERO Defense Systems, split evenly between cash and stock. Koranda said HERO’s aerosol pepper gel device and compact nitrogen-powered launcher fit Byrna’s strategy of expanding its less-lethal product assortment.

Koranda expects Byrna to generate negative Adjusted EBITDA of $1.4-million on revenue of $88.7-million in fiscal 2026, improving to Adjusted EBITDA of $1.4-million on revenue of $93.9-million in fiscal 2027.

-30-

Rod Weatherbie

Writer

Rod Weatherbie is a journalist based in Prince Edward Island. Since 2004, he has written extensively about the Canadian property and casualty insurance landscape. He was also a founder and contributing editor for a Toronto-based arts website and a PEI-based food magazine. His fiction and poetry have been featured in The Fiddlehead, The Antigonish Review, and Juniper.

Related Posts

Roth Capital Markets analyst Matt Koranda maintained his “Buy” rating on Byrna Technologies (Byrna Technologies Stock Quote, Chart, News, Analysts,...