CAE stock is too expensive right now, Barry Schwartz says

Looking for a company that’s superbly positioned in a growing industry? Portfolio manager Barry Schwartz says flight simulator and training company CAE (CAE Stock Quote, Chart, News TSX:CAE) fits the bill.

The only problem? The stock’s too expensive right now.

Montreal’s CAE has seen its share price take off over the past few years, in concert with the growing demand for air travel and air cargo services. Taking a flight may not be the most comfortable few hours of your life but with tickets being relatively affordable and, globally, more and more people reaching a level of affluence allowing for air travel, the passenger industry is on a high right now, not to mention the current obsession with speedy (hence, in the air) shipping which has fuelled the cargo business.

And while the airlines make for notoriously tricky investments, there may be less volatility found in a company like CAE, whose flight simulators and pilot-training programs are in demand.

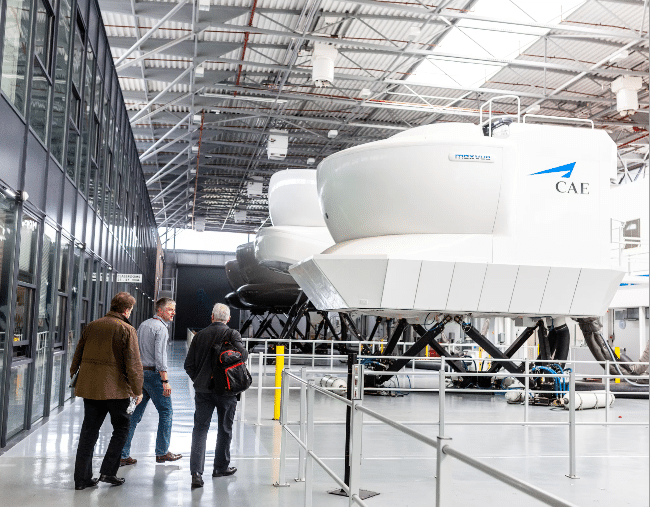

Last week, the company announced that it is preparing for increased demand for its flight simulators for the currently grounded Boeing 737 Max, saying that it has delivered 19 of 48 737 Max simulators on order so far.

Schwartz, chief investment officer at Baskin Wealth Management, says that CAE is in the right place at the right time.

“This is a stock that we used to own many years ago. We probably bought it at $8 and sold it at $9, and now the stock is $35,” said Schwartz, in conversation with BNN Bloomberg on Tuesday.

“It’s riding the tailwind of aviation and travel explosion of business and leisure travel. I read that the company just ordered a number of simulators to retrain the pilots on the Boeing 737 Max,” he says.

“This is a great business in that all of the airlines don’t want to insource the flight simulation training. It’s better just to outsource it, and CAE is going to benefit,” Schwartz says.

CAE’s share price jumped last week on the company’s second quarter earnings, which beat expectations for both revenue and profit. The company reported a top line of $896.8 million, up from $743.8 million a year ago, and net income attributable to shareholders of $73.8 million or $0.28 per share, up from $60.7 million or $0.23 per share a year prior. Analysts had been expecting a profit of $0.25 per share on $849.9 million in revenue.

“CAE had good growth in the second quarter, with 21 percent higher revenue and 28 percent higher operating income, and we secured nearly $1.0 billion of orders for a $9.2 billion backlog,” said Marc Parent, CAE’s President and CEO, in a press release. “Performance was led by Civil with 60 percent operating income growth and higher margins, and continued good momentum signing long-term training agreements with our airline partners.”

Schwartz said that investors may want to hold off on the stock, which has gained 41 per cent year-to-date.

“On a valuation basis, it looks kind of expensive for the growth that you’re getting. I wouldn’t be in a rush to buy it,” says Schwartz. “I read recently that Boeing expect travel and business travel to double over the next ten years and so we’re going to need a lot more planes and a lot more pilots, and CAE should benefit from that going forward.”

Nick Waddell

Founder of Cantech Letter

Cantech Letter founder and editor Nick Waddell has lived in five Canadian provinces and is proud of his country's often overlooked contributions to the world of science and technology. Waddell takes a regular shift on the Canadian media circuit, making appearances on CTV, CBC and BNN, and contributing to publications such as Canadian Business and Business Insider.

Related Posts

National Bank Financial analyst Cameron Doerksen raised his target on CAE (CAE Stock Quote, Chart, News, Analysts, Financials TSX:CAE) to...

Desjardins Securities analyst Benoit Poirier has become a little more bullish on CAE (CAE Stock Quote, Chart, News, Analysts, Financials...