Perimeter Medical Imaging wins price target raise from this analyst

In an April 8 note, Paradigm Capital analyst Scott McAuley maintained his “Speculative Buy” rating on Perimeter Medical Imaging AI (Perimeter Medical Imaging AI Stock Quote, Chart, News, Analysts, Financials TSXV:PINK) and raised his target to C$0.95 from C$0.70 after fourth-quarter results and recent M&A activity in breast cancer surgery.

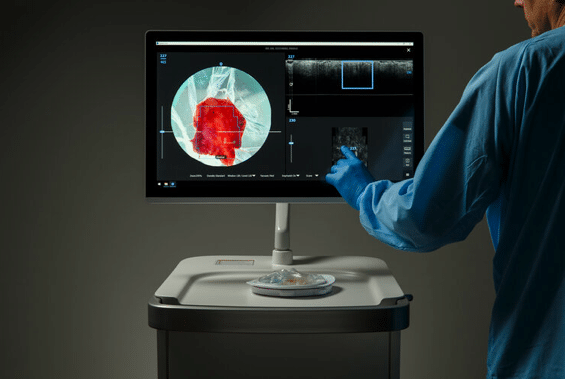

McAuley said Perimeter’s FDA-cleared Claire device addresses a significant unmet need in breast-conserving surgery, where about 20% of the 200,000 annual U.S. lumpectomies require a second operation because cancer is missed the first time.

The analyst said Claire uses specialized algorithms to analyze OCT images during surgery and give surgeons real-time guidance on whether more tissue should be removed. With recurring revenue from disposables and potential expansion beyond breast cancer, he said Perimeter offers a compelling medtech growth story.

Perimeter reported fourth-quarter revenue of $711,000, below McAuley’s $880,000 estimate, but still up 145% year over year and 32% sequentially. Consumables revenue of $442,000 pointed to stronger utilization even before approval of the next-generation system. Adjusted EBITDA was negative $1.7-million, better than McAuley’s negative $2.3-million forecast, helped by higher-than-expected gross margin of 76% and lower operating costs of $2.5-million. He said the revenue shortfall was mainly due to the absence of capital sales in the quarter.

McAuley said the main near-term issue is the balance sheet. Perimeter ended the year with $2.5-million in cash after using $1.4-million in operating cash during the quarter, and he estimates the company would need about $10-million to fund 12 to 18 months of runway as it builds out its sales and clinical teams and inventory. He also noted that $5.3-million of warrants at a $0.35 strike, outstanding until 2030, could become both a source of capital and an overhang.

“Overcoming the balance sheet overhang in the near term will help give the market confidence that PINK has the firepower to execute on the first stage of commercial expansion,” he said.

Commercially, McAuley said Perimeter has about 23 S-Series systems installed in U.S. hospitals, which should form the initial base for Claire adoption. He added that the timing of Claire’s approval is favourable ahead of the American Society of Breast Surgeons meeting in Seattle from April 29 to May 3, where he expects the company to have a strong presence. He also said Claire’s Breakthrough Device Designation should help support transitional pass-through payments ahead of full Medicare reimbursement.

McAuley also pointed to recent M&A as a sign of growing strategic interest in breast cancer surgery technology. He said Merit Medical’s April 1 agreement to buy private View Point Medical for $140-million valued that company at roughly 35 times 2026 revenue and 9.3 times 2027 revenue, while earlier deals involving Molli Surgical and Endomag suggest larger strategic buyers are active in the space. In his view, margin assessment tools such as Claire could be the next focus.

McAuley said Perimeter should post an Adjusted EBITDA loss of $8.0-million on revenue of $5.1-million in fiscal 2026, followed by an Adjusted EBITDA loss of $8.2-million on revenue of $12.2-million in fiscal 2027.

He said his new C$0.95 target is based on 9.0 times projected 2027 revenue, using M&A multiples for growth medtech companies.

-30-

Rod Weatherbie

Writer

Rod Weatherbie is a journalist based in Prince Edward Island. Since 2004, he has written extensively about the Canadian property and casualty insurance landscape. He was also a founder and contributing editor for a Toronto-based arts website and a PEI-based food magazine. His fiction and poetry have been featured in The Fiddlehead, The Antigonish Review, and Juniper.

Related Posts

Leede Financial analyst Douglas Loe reiterated his “Speculative Buy” rating and $3.00 target price on Perimeter Medical Imaging (Perimeter Medical...

Paradigm Capital analyst Scott McAuley maintained a “Speculative Buy” rating but lowered his target price for Perimeter Medical Imaging AI...