This analyst loves Zedcor

On Dec. 11, Ventum Capital Markets analyst Amr Ezzat initiated coverage of Zedcor with a “Buy” rating and a 12-month target price of C$8.70, implying roughly 47.5% upside from current levels.

Ezzat said the stock’s recent re-rating has pulled investor focus toward near-term estimates, while obscuring what he views as the more compelling long-duration value in the model.

“We believe the market is focused on the wrong part of the curve,” he said, arguing that consensus forecasts are now running ahead of what the network can deliver without several large marquee contract wins. In his view, those wins remain possible but are not required for long-term value creation.

“The deeper inefficiency lies on the long end of the curve,” he said, as Zedcor remains in an intensive build phase where consolidated returns understate the economics of individual assets.

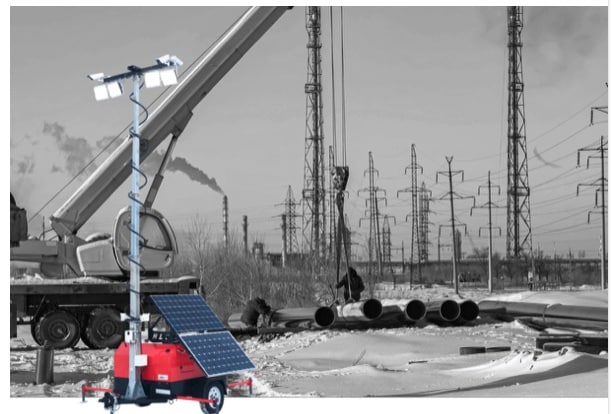

Calgary-based Zedcor provides mobile security and surveillance services to enterprise and public-sector customers across North America, operating a growing network of surveillance towers supported by in-house monitoring and standardized hardware.

Ezzat highlighted that reported returns remain depressed by reinvestment intensity, with consolidated ROIC of roughly 7.8% masking materially stronger unit economics. Each tower, he said, typically pays back in under two years, generates approximately 65% tower-level margins, and requires limited ongoing maintenance. As reinvestment normalizes and scale efficiencies flow through the cost structure, Ezzat expects consolidated ROIC to move toward 16–17% over the next four years.

He also emphasized the durability of Zedcor’s revenue base, which he said is driven more by operating efficiency than by contract mechanics. As network density increases, Ezzat expects route efficiency, redeployment cycles, and branch-level margins to continue improving, with U.S. regions showing higher utilization and Canada’s mature footprint delivering stronger EBITDA margins.

From a forecasting standpoint, Ezzat initiated his 2026 revenue estimate at C$100.2-million, below the low end of consensus, which stands at C$109.8-million. He said any near-term estimate resets would be viewed as opportunities within a bullish long-duration thesis.

“Any pullbacks tied to short-term forecast resets would, in our view, create opportunities,” he said.

He said that insider ownership of roughly 23% reinforces alignment around disciplined capital allocation as the company scales.

Ezzat said Zedcor should generate C$21.3-million in Adjusted EBITDA on C$59.1-million of revenue in fiscal 2025, improving to C$38.3-million of EBITDA on C$100.2-million of revenue in fiscal 2026.

-30-

Tara Whittet

Writer

Tara Whittet is Senior Sales Manager at Cantech Letter.