Tons of upside to Cellectar Biosciences, says Roth

Biotech stock Cellectar Biosciences (Cellectar Biosciences Stock Quote, Charts, News, Analysts, Financials NASDAQ:CLRB) has fallen a long way over the past couple of years, but Roth Capital Partners analyst Jonathan Aschoff sees room for improvement. Aschoff reiterated a “Buy” rating on Cellectar in a Monday note to clients, where he reviewed the latest clinical findings from the company.

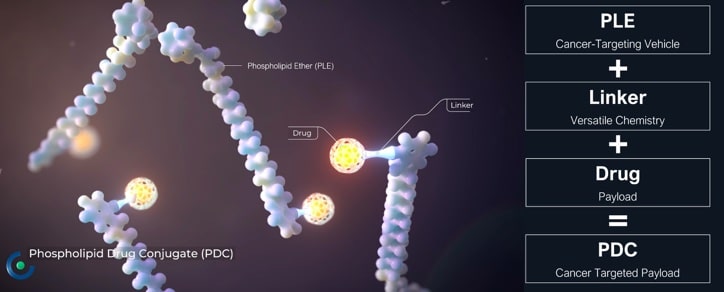

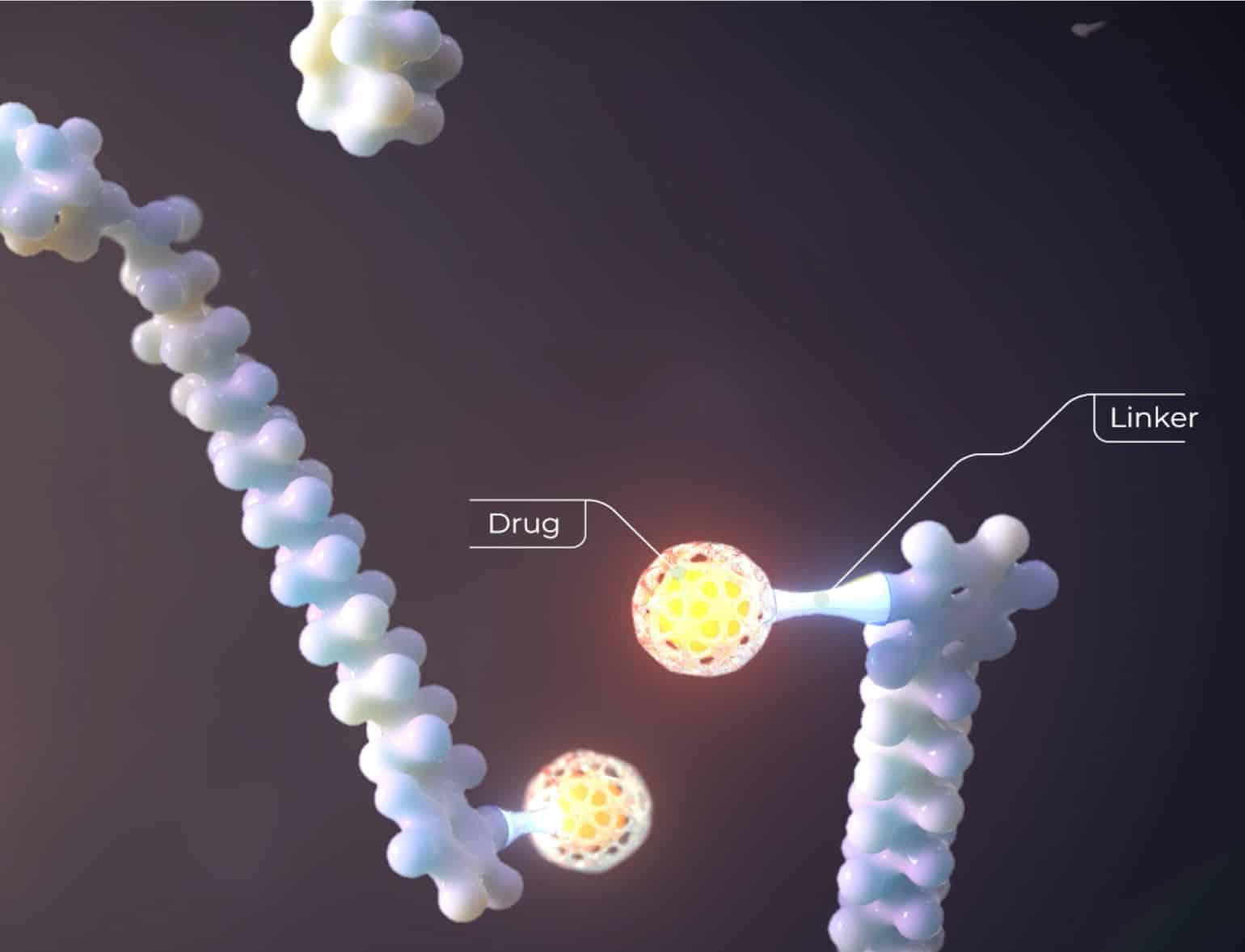

Cancer drug development company Cellectar announced on November 21 preclinical data in support of its CLR 12120 series of targeted alpha-emitting therapies and highlighting the company’s phospholipid ether cancer cell targeting platform. Cellectar has the proprietary Phospholipid Drug Conjugate (PDC) delivery platform for targeting cancer cells with improved efficacy and better safety results.

Cellectar said the preclinical data show high tumour delivery with low off-target uptake on the CLR compounds when administered as monotherapies. The company also said that mouse model data showed a therapeutic efficacy of all three CLR 12120 candidates at both single and multiple doses in preclinical pancreatic and triple negative breast cancer xenograft models.

“The data from our CLR 12120 series is highly encouraging and further validates the payload versatility and precision targeting of our PLE delivery platform,” said Jarrod Longcor, Cellectar’s Chief Operating Officer, in a press release.

“The data confirm the ability of the PLEs to deliver nearly any radioisotopes including alpha- and beta-emitters directly to tumour cells. Furthermore, the efficacy data demonstrate the potential to treat highly aggressive and difficult to treat cancers and provides additional future clinical development considerations,” he said.

Cellectar’s share price was travelling in the $120 range as recently as 2018 but it fell back to around $20 for a while before skidding further over 2021 and 2022. Currently around the $2 mark, CLRB has a year-to-date return of negative 70 per cent. (All figures in US dollars.)

But Aschoff sees a lot of upside over the next 12 months, reiterating with his “Buy” rating a $25.00 target price on the stock, which at the time of publication represented a projected return of 1,202 per cent.

“We look forward to CLRB releasing more preclinical results with this series of compounds and to its choice of what to ultimately bring into the clinic,” Aschoff wrote.

Aschoff’s said his valuation on CLRB is based on the potential of CLR 131, a small-molecule PDC for the targeted delivery of iodine-131 directly to cancer cells, for the treatment of multiple myeloma and LPL/WM in the United States.

Jayson MacLean

Writer

Jayson is a writer, researcher and educator with a PhD in political philosophy from the University of Ottawa. His interests range from bioethics and innovations in the health sciences to governance, social justice and the history of ideas.

Related Posts

Roth Capital Markets analyst Jonathan Aschoff lowered his price target on Cellectar Biosciences (Cellectar Biosciences Stock Quote, Chart, News, Analysts,...