Cargojet has a 63 per cent upside, says Beacon

Results were mixed for the third quarter for Canadian overnight freight company Cargojet (Cargojet Stock Quote, Charts, News, Analysts, Financials TSX:CJT), according to Beacon Securities analyst Ahmad Shaath, who reviewed the results in an update to clients on Monday. Shaath reiterated a “Buy” rating on the stock, saying Cargojet’s domestic revenues are proving resilient, while its airplane leasing business continues to grow.

Mississauga-based air cargo services company Cargojet announced its third quarter 2022 financials on Monday, showing revenues up 23 per cent to $232.7 million and adjusted EBITDA of $82.1 million

“Over the past several years, Cargojet has evolved its business model that is increasingly based on strategic partnerships rather than transactional relationships with its customers. By aligning our long-term commercial interests, we expect greater endurance of volumes with our strategic customers even if global volumes soften during a recessionary period,” said Dr. Ajay Virmani, President and CEO, in a press release.

Looking at the Q3 numbers, Shaath said Cargojet’s topline of $232.7 million was below expectations, where Shaath had forecasted $253 million and the consensus call was for $245 million. Adjusted EBITDA of $82 million was also under expectations, with Shaath at $87 million and the Street at $85 million.

Shaath said Cargojet’s revenue growth appeared to be mainly driven by volume, with price effects, including CPI-related adjustments being minimal. ACMI (aircraft, crew, maintenance and insurance leasing) revenues of $66 million, meanwhile, were slightly ahead of Shaath’s estimate at $63 million, which helped to offset weakness in CJT’s ad-hoc charter revenue.

“On the [conference] call, management noted that normal seasonal trends and double-digit growth are expected in Q4/FY22E. Conversations with customers are focused on the peak season and there hasn’t been any meaningful discussion for FY23E volumes. As of today, we believe mid-single-digit growth in the domestic network is reasonable for FY23E,” Shaath wrote.

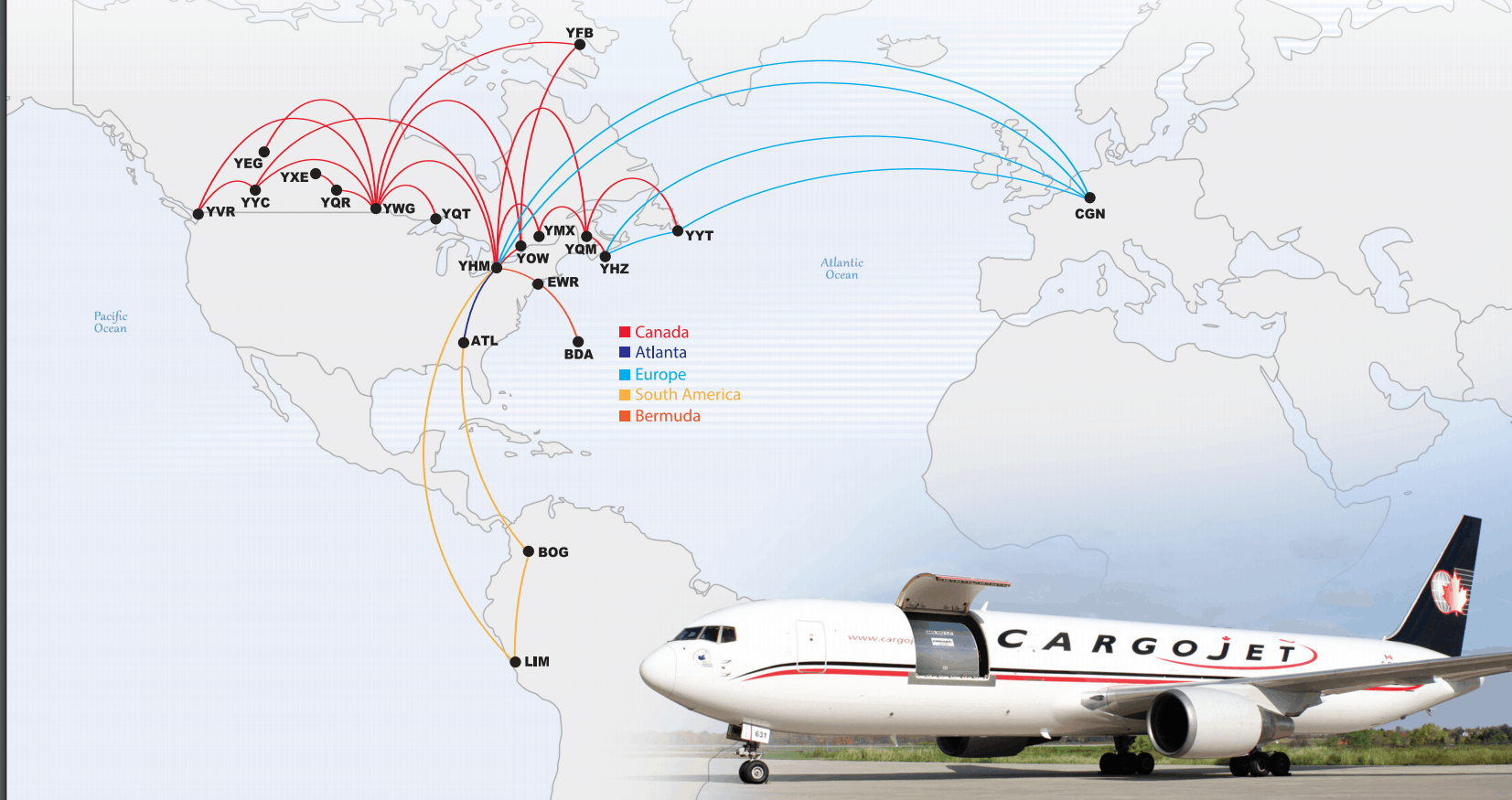

Shaath said the outlook for CJT’s ACMI business looks solid, with the company continuing to add new routes. The analyst noted a new route expected to start this week connecting Europe to Los Angeles through Halifax along with an additional B757 route to come in the second quarter of 2023.

With the new results, Shaath adjusted his forecast for CJT and is now calling for full 2022 revenue and EBITDA of $984.0 million (previously $1,029.0 million) and $348.0 million (previously $355.0 million), respectively. For 2023, the call is for $1,037.0 million in revenue (previously $1,046.0 million) and $374.0 million in EBITDA (previously $384.0 million).

“We tweaked our forecast to reflect further slowdown in ad-hoc revenues, offset by higher ACMI revenue (to reflect the new, longer route), with our domestic network forecasts unchanged. The impact on profitability is largely a function of smaller benefit on fuel pass through and the reduction in ad-hoc charter revenues, with ACMI growth (~70 per cent EBITDA margin) offsetting most of these headwinds,” Shaath wrote.

With his maintained “Buy” rating, Shaath has also left his $220.00 price target unchanged, implying a one-year return of 63 per cent.

Jayson MacLean

Writer

Jayson is a writer, researcher and educator with a PhD in political philosophy from the University of Ottawa. His interests range from bioethics and innovations in the health sciences to governance, social justice and the history of ideas.

Related Posts

“Clearer Skies Ahead”. That’s the overall assessment of Cargojet (Cargojet Stock Quote, Chart, News, Analysts, Financials TSX:CJT) from Paradigm Capital...

Following the company’s fourth quarter results, Beacon analyst Donangelo Volpe has maintained his “Buy” rating on Cargojet (Cargojet Stock Quote,...