After quarterly earnings from oil and gas software company Computer Modelling Group (Computer Modelling Group Stock Quote, Charts, News, Analysts, Financials TSX:CMG), Echelon Capital Markets analyst Amr Ezzat is a little more positive on the stock but not enough to move the needle. In a report to clients on Wednesday, Ezzat maintained his “Hold” rating while upping his target price from $4.75 to $5.50, saying there’s likely limited upside over the next while.

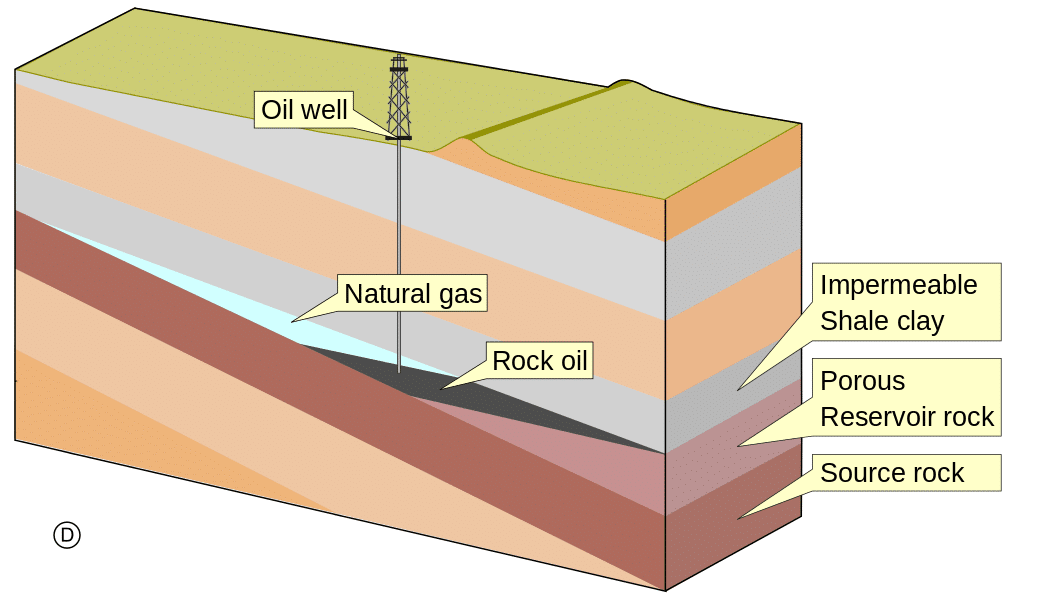

Calgary-based CMG, which develops and licenses reservoir simulation software and has over 550 clients across 58 countries, announced on Wednesday its financials for the three and six months ended September 30, showing fiscal 2022 second quarter revenue of $15.9 million compared to $17.9 million a year earlier and $14.4 million for the previous quarter. The company said the 11 per cent year-over-year slide was due to drops in software licensing and professional services revenue. Total software license revenue decreased in all the company’s geographic regions. CMG get the majority of its revenue from software license sales comprising about 87 per cent of the total last fiscal year while Professional services revenue accounted for 13 per cent. Software license revenue breaks down into Annuity/maintenance license revenue and Perpetual license revenue.

The company said it ended the quarter in a strong financial position with $48.0 million in cash and no debt and that it generated free cash flow over the quarter of $0.06 per share and paid out dividends of $0.05 per share over the fiscal Q2.

CMG also said that energy transition-related modelling for processes such as carbon capture and sequestration and EOR, hydrogen, geothermal and others has been a “bright spot” for the company over the past year and a half, with the current macro focus on energy transition creating more opportunities for the company which could have value for decades to come.

“Although our results are impacted by the ongoing headwinds associated with the COVID-19 pandemic, we are seeing recovery in both oil and gas demand and commodity prices. As market sentiment improves and our customers adapt to operating in volatile market conditions, we are focused on returning to growth by working with our customers in their upcoming annual budget cycles to provide them with needed solutions,” the company said in a press release.

“As the market focuses on energy transition, capital discipline, operational efficiencies and debt reduction, CMG will be responsive and proactive to our customers’ needs and will support them in improving the value of their assets by optimizing production and realizing operational cost efficiencies,” CMG said.

Overall, annuity and maintenance license revenue dropped by six per cent for the quarter and total operating expenses grew by 32 per cent year-over-year and quarterly operating profit margin was 34 per cent.

Looking at the numbers, Ezzat said the $15.9 million in sales was above his call for $14.9 million and the Street’s forecast for $15.5 million while the fiscal Q2 EBITDA of $6.5 million (representing a 40.6 per cent margin) was also better than his $6.0 million estimate but below the consensus call for $7.2 million. Ezzat said the quarterly earnings were impacted by higher opex related to a one-time restructuring charge of $0.9 million taken in the quarter. The analyst said that excluding that charge, CMG’s EBITDA margin would have been about 46 per cent.

“FQ222 results reflect a more supportive environment with Annuity & Maintenance (A&M) licenses (recurring revenues) down 8.6 per cent year-over-year on a normalized basis while deferred revenues increased for the first time since FQ320, up 8.7 per cent year-over-year,” Ezzat wrote.

“While we remain fans of CMG and are encouraged by CoFlow commercialization activity, we expect the stock to be range-bound with our 12-month target price of $5.50/share (up from $4.75/share) implying limited upside from current levels. We believe a higher return profile is possible beyond our target price should oil prices remain constructive for a sustained period,” Ezzat said.

By his revised forecast, Ezzat is now calling for CMG to generate full fiscal 2022 revenue and EBITDA of $62.6 million and $27.8 million, respectively, with EPS coming in at $0.20 per share. At the time of publication, his new $5.50 target represented a projected total one-year return of 6.9 per cent. Ezzat said CMG’s shares are currently trading at 6.1x fiscal 2022 sales and at 13.7x 2022 EBITDA.

After finishing 2020 with CMG’s stock down 41 per cent, the company’s share price is currently up about ten per cent.

Over the quarter, Computer Modelling Group signed a multi-year agreement for CoFlow annuity licensing which it called the largest agreement for CoFlow commercial use to date. CoFlow is the company’s reservoir and production system simulation software.

About The Author /

Jayson is a writer, researcher and educator with a PhD in political philosophy from the University of Ottawa. His interests range from bioethics and innovations in the health sciences to governance, social justice and the history of ideas.

Leave a Reply

You must be logged in to post a comment.

RELATED POSTS

Share

Share Tweet

Tweet Share

ShareTRENDING

All Trending →

TTNM keeps “Buy” rating at Haywood

March 20, 2024

NEO stock has price target chopped at Paradigm

March 18, 2024

Groupon’s turnaround is accelerating, Roth says

March 18, 2024

Comment