Sell your Maxar stock? I wouldn’t, says this investor

Even with all its gains this year, there’s still room to grow for space tech company Maxar Technologies (Maxar Technologies Stock Quote, Chart, News, Analysts TSX:MAXR), says portfolio manager John Zechner, who claims the stock is still trading at a reasonable valuation.

“We’re still hanging on,” says Zechner, chairman and founder of J. Zechner Associates, speaking on BNN Bloomberg on Tuesday. “We’ve had a great run on this stock. I think it started the year around C$6 or C$7 and now it’s in the mid-C$40s.”

Maxar’s troubles started surfacing a few years ago when the stock tanked due to concerns about the viability of its business. Maxar, which counts satellite, robotics, imaging, data and analytics among its offerings, had been dealing with an unwieldy debt load and low-profit contracts when it suffered a few body blows, first in the form of a short-seller attack in 2018 questioning its accounting, then a write-down of its satellite business and, at the start of 2019, the loss of one of its imaging satellites due to malfunction. All of which made the stock a no-go zone from the market’s point of view and pulled MAXR’s share price from C$80 to sub-C$10 territory by early 2019.

Yet the company’s more recent moves seem to have been to the liking of investors, as the stock rose 29 per cent in 2019 and is now up 118 per cent for 2020.

That turnaround has been chalked up to, among other things, better debt management through the restructuring of some of its debt but also from Maxar’s reducing some of that leverage via offloading MDA, the Canadian arm of its business, to a consortium of Canadian investors, a deal which concluded this past April. Maxar said the sale MDA plus the selling some real estate in Palo Alto allowed the company to shave a full $1 billion from its debt.

“The closing of the MDA transaction concludes the near-term reshaping of our balance sheet and business portfolio,” said Dan Jablonsky, Maxar CEO, in an April 8, 2020, press release. “Going forward, our growth strategy remains focused on providing leading capabilities in Earth Intelligence and Space Infrastructure, including geospatial data, data analytics and spacecraft and robotics that are well aligned with the strategic priorities of our government and commercial customers.”

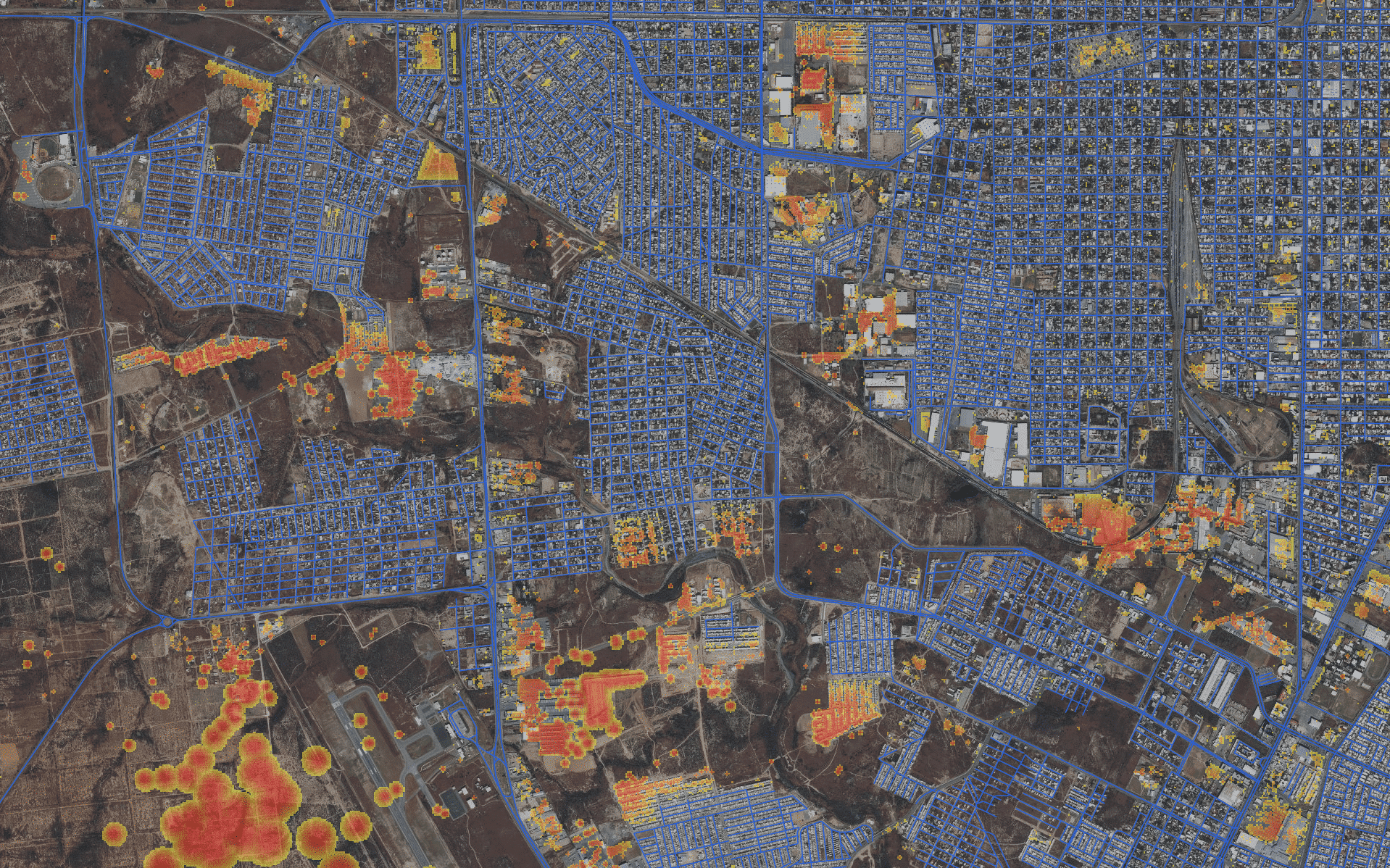

Shedding MDA left Maxar with a focus on its space imagery business under DigitalGlobe, acquired in 2017, and Zechner says that’s an industry where Maxar can really flourish going forward.

“I think their acquisition of DigitalGlobe — which I think made a ton of sense — really put the stock under a lot of pressure and people worried about the balance sheet, people worried about the future the satellites,” Zechner said. “And now, with this whole move to you could call it the space race again but certainly the more industrialization of space, I think Maxar are coming to the forefront as a great play.”

“What the DigitalGlobe acquisition gave them was the ability to marry their own production of orbital satellites with the software to analyze the data, which we know is becoming core, not only for the military and defence but for urban planning, for security and for a whole host of other reasons,” Zechner added.

“You’re looking at data from outer space as being a lot more accurate and a lot more definable, and these guys have the ability to derive it, synthesize it, assimilate and provide it to industry, to governments,” he said.

Maxar’s share price had a momentary drop in early November after the company’s most recent quarterly numbers, its third quarter 2020, came up lighter than expected and the company’s forecast for the 2020 year was decreased, calling for revenue to be flat across its Earth Intelligence and Space Infrastructure segments. Management also said there would be a potential delay in the launch of its WorldView Legion program of next-generation Earth imaging satellites.

National Bank Financial analyst Richard Tse called the third quarter results soft and said there are a lot of moving parts involved in Maxar’s resurgence, noting in particular an execution risk attached to WorldView Legion. Tse delivered an update to clients on November 5 where he left his “Sector Perform” rating unchanged for MAXR while dropping his target price from US$30.00 to US$28.00, which at the time of publication represented a projected 12-month return of negative 1.9 per cent.

Zechner maintains investors who have done well with Maxar through 2020 might want to stick around.

“Also, it’s only trading about 8x operating cash flow and the balance sheet is starting to get in better shape here, they’re going to start to pay down the debt and they’ve got that low-orbit digital satellite system going out in the next year,” Zechner said. “So, I’m still hanging on despite the fact that it’s had a huge move this year.”

Nick Waddell

Founder of Cantech Letter

Cantech Letter founder and editor Nick Waddell has lived in five Canadian provinces and is proud of his country's often overlooked contributions to the world of science and technology. Waddell takes a regular shift on the Canadian media circuit, making appearances on CTV, CBC and BNN, and contributing to publications such as Canadian Business and Business Insider.

Related Posts

The space race is on and Maxar Technologies (Maxar Technologies Stock Quote, Chart, News, Analysts, Financials NYSE:MAXR), a down-and-out stock...

The past couple of years have been rough on the nerves for shareholders of Maxar Technologies (Maxar Stock Quote, Chart,...