Is CargoJet is a better eCommerce play than Shopify?

CargoJet over Shopify? When you take into account their relative valuations the former is compelling, says one investor.

It’s a case of look before you leap with Shopify (Shopify Stock Quote, Chart, News TSX:SHOP), says portfolio manager Bryden Teich, who feels that although the e-commerce company is a bona fide Canadian tech darling, the stock is way too expensive right now.

Shopify’s share price is down just one per cent in midday Tuesday trading after the e-commerce company released its fiscal third quarter financials. The company posted quarterly revenue of $390.6 million, a full 45-per-cent increase year-over-year and better than the consensus expectation of $384 million, with the company saying that it has shot past the one million mark in merchants using its platform. (All figures in US dollars.)

“More than a million merchants are now building their businesses on Shopify, as more entrepreneurs around the world reach for independence,” said CEO Tobi Lütke, in a press release. “These merchants chose Shopify because we’re making entrepreneurship easier, and we will continue to level the playing field to help merchants everywhere succeed.”

Yet the quarter also featured a net loss of $72.8 million or 64 cents per share, much higher than the $23.2 million or 22 cents per share net loss from a year ago. An adjusted earnings loss of 25 cents ended up below analysts’ consensus estimated loss of 11 cents.

After zooming up the charts this year, the stock has pulled back over the past couple of months while still remaining up over 130 per cent for the year.

Teich says that the reason why the market doesn’t appear to appreciate SHOP’s consistently strong revenue numbers (the Q3 2019 amounted to the 17th in a row where it beat the consensus estimate on revenue) is that growth stories like Shopify are all about surpassing expectations.

“Shopify has definitely performed well this year but it has also been incredibly volatile going back the last several years,” says Teich, partner and portfolio manager at Avenue Investment Management, to BNN Bloomberg on Monday. “Traditionally, around earnings time the expectations are so high for a name like this, so you really need a big surprise beat or some really, really good news that isn’t priced into a stock that has already gone up 100 per cent this year.”

“It’s hard to do that every quarter, so it’s not a name that I would be trying to buy right before the quarter. You may have the shares react positively, but as an investor you just have to be okay with missing out on something like that.’ Teich says.

“The issue with Shopify is that because there are so few technology companies in Canada if you are a large mutual fund or an index-weighted mutual fund and you have to have some technology — all of those people are in Shopify because you get size, you get growth and you get liquidity. So, sometimes these market effects will push a name up much higher than it probably should go. And so, at the valuation that it has right now it’s not a name that we would be looking at,” he says.

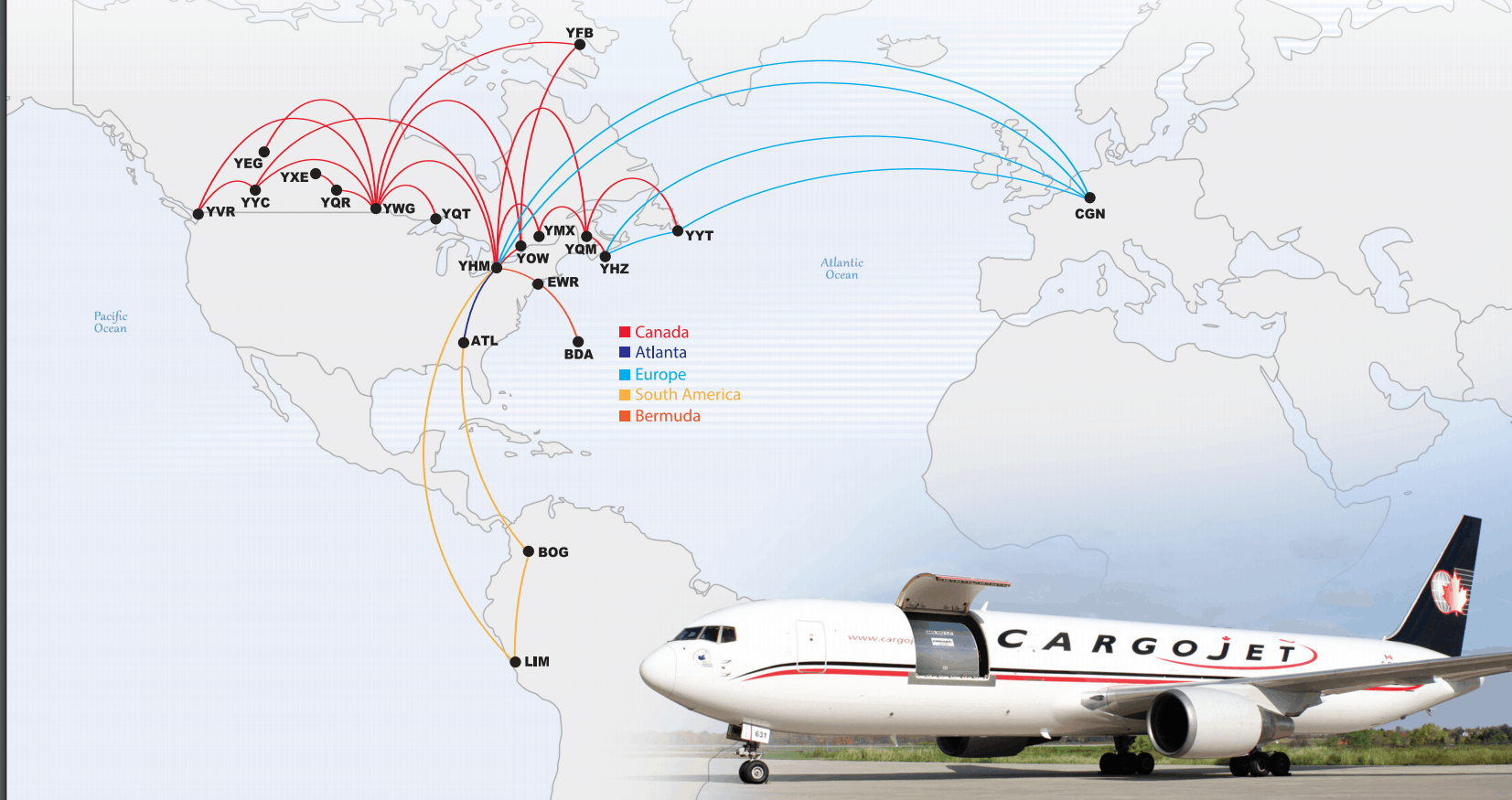

As far as the Canadian eCommerce play goes, Teich likes overnight air cargo company CargoJet (CargoJet Stock Quote, Chart, News TSX:CJT), which recently announced a big partnership deal with Amazon where the latter has agreed to become a shareholder in CargoJet in time.

“The lingering concern with CargoJet going back over the last year was whether Amazon was going to partner with someone else, as Amazon has really wreaked havoc among UPS and FedEx in the US. But now that Amazon is onside, really, this is the clearest way to play e-commerce in Canada in a company that’s doing other things as well,” Teich says.

Jayson MacLean

Writer

Jayson is a writer, researcher and educator with a PhD in political philosophy from the University of Ottawa. His interests range from bioethics and innovations in the health sciences to governance, social justice and the history of ideas.

Related Posts

“Clearer Skies Ahead”. That’s the overall assessment of Cargojet (Cargojet Stock Quote, Chart, News, Analysts, Financials TSX:CJT) from Paradigm Capital...

Following the company’s fourth quarter results, Beacon analyst Donangelo Volpe has maintained his “Buy” rating on Cargojet (Cargojet Stock Quote,...