CargoJet stock has an upside of 27 per cent: Echelon

Following the company’s second quarter results, Echelon Wealth Partners analyst Gianluca Tucci has maintained his “Buy” rating on CargoJet (CargoJet News, Stock Quote, Chart TSX:CJT)

This morning, CargoJet reported its Q2, 2019 results. The company posted Adjusted EBITDA of $37.5-million on revenue of $119.1-million, a topline that was up 9.3 per cent over the same period last year.

“A strong financial discipline combined with continued strength in our core business allowed us to post another strong quarter,” CEO Ajay Virmani said. “As the courier industry shifts to [a] seven-day-a-week delivery model to accommodate faster service expectations of e-commerce retailers, we are uniquely positioned to execute on this new model. We are also finding growing synergistic opportunities in our ad hoc and ACMI charter business that is improving fleet utilization and overall margins. At the heart of our strategy is service excellence and I am extremely proud of Cargojet team that continues to exceed customer expectation by delivering unprecedented on-time performance.”

Tucci notes that the results were better than his expectations and continues to believe CargoJet is undervalued.

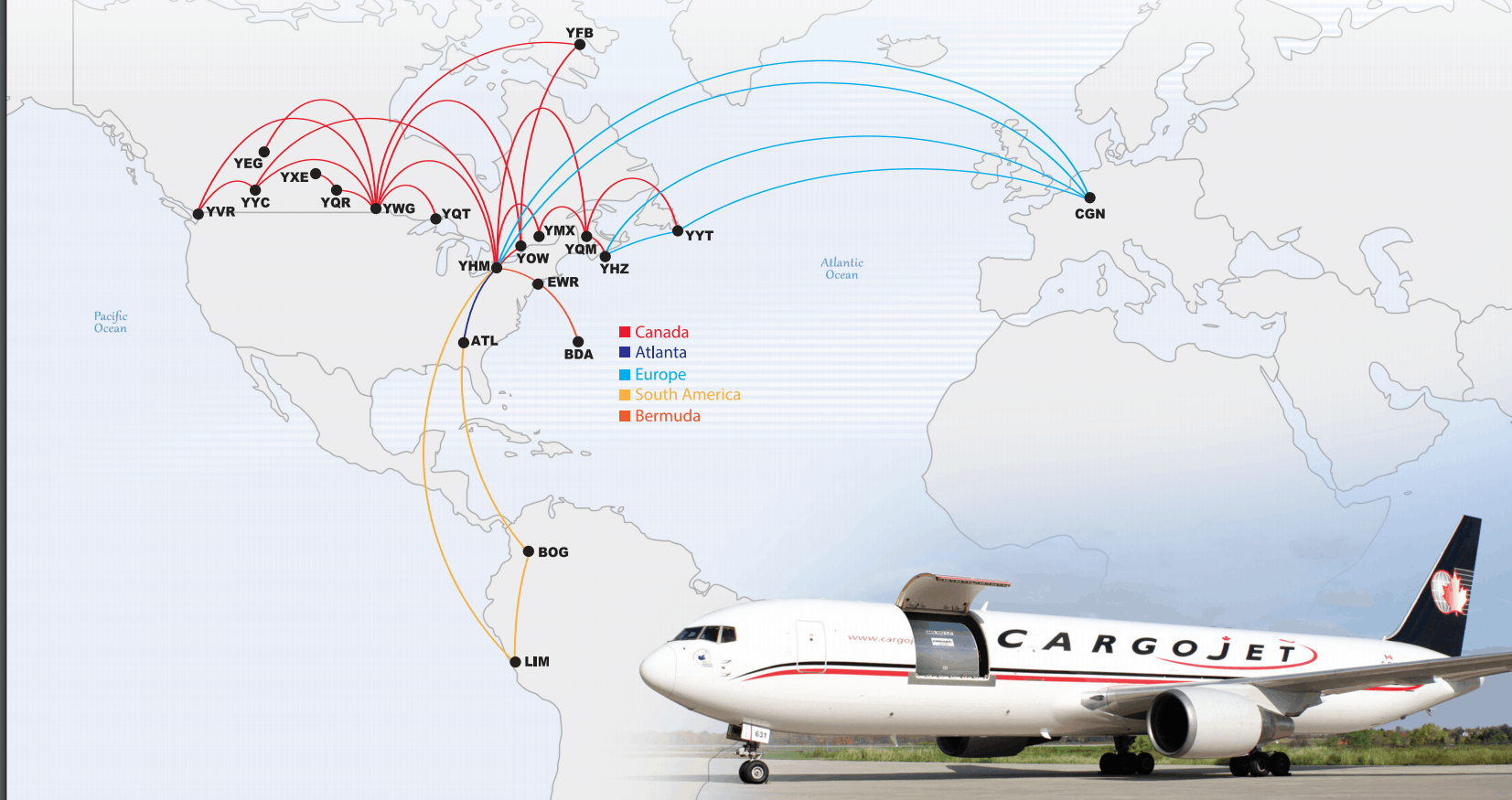

“Canada has a very unique geography, which creates a special opportunity for CJT, ” the analyst writes. “A natural monopoly exists given Canada’s large and sparse footprint and first-mover advantage has created a sustainable competitive advantage with the regulatory environment providing further support for CJT: foreign ownership and cabotage laws restrict foreign freight airlines from flying between airports within Canada (cabotage is the transport of goods or passengers between two points in the same country by an aircraft registered in another country). CJT and Canada Post entered into an agreement on April 1, 2015, that resulted in CJT becoming the exclusive provider of time-sensitive airfreight services to Canada Post. On October 23, 2017, the original Master Services Agreement (MSA) was extended by three years to March 31, 2025 (with two additional 3-yr extensions remaining). Coupled with other long-term customer contracts, the majority of CJT’s revenues are de-risked. With e-commerce representing less than 10% of total Canadian retail sales (ex-motor vehicles and gasoline sales), we believe this secular shift remains in its very early innings. CJT remains one of the prime beneficiaries of this secular shift to e-commerce from brick-and-mortar.”

CargoJet stock is undervalued, the analyst says

In a research update to clients today, Tucci maintained his “Buy” rating and one-year price target of $120.00 on CargoJet, implying a return of 27 per cent at the time of publication.

Tucci thinks CJT will post Adjusted EBITDA of $152-million on revenue of $498-million in fiscal 2019. He expects those numbers will improve to EBITDA of $172-million on revenue of $538-million the following year.

Nick Waddell

Founder of Cantech Letter

Cantech Letter founder and editor Nick Waddell has lived in five Canadian provinces and is proud of his country's often overlooked contributions to the world of science and technology. Waddell takes a regular shift on the Canadian media circuit, making appearances on CTV, CBC and BNN, and contributing to publications such as Canadian Business and Business Insider.

Related Posts

“Clearer Skies Ahead”. That’s the overall assessment of Cargojet (Cargojet Stock Quote, Chart, News, Analysts, Financials TSX:CJT) from Paradigm Capital...

Following the company’s fourth quarter results, Beacon analyst Donangelo Volpe has maintained his “Buy” rating on Cargojet (Cargojet Stock Quote,...