Why Sameet Kanade is RIM’s most pessimistic analyst

Yesterday, in a research update to clients, Northern Securities analyst Sameet Kanade issued a SELL recommendation on Research in Motion and lowered his target price on the stock. Kanade’s prior target of $6 was on the low end of the spectrum, but his new target price of $4.50 became the street’s most pessimistic assessment of the BlackBerry maker’s business.

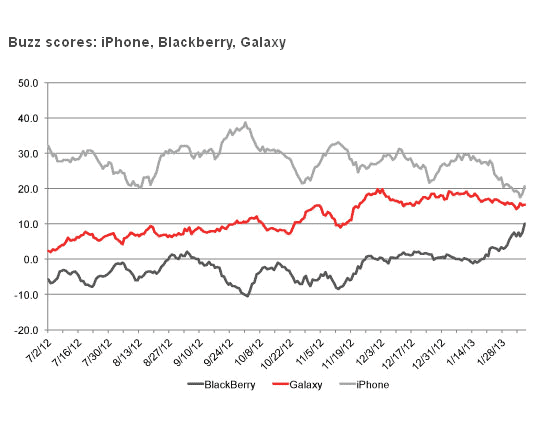

So what prompted Kanade to change his rating from HOLD to SELL? He says while we wait for the company’s new BlackBerry 10 platform, the landscape RIM will resurface into has become hyper-competitive. Kanade points to the successful launches of the iPhone 5 and the Samsung Galaxy SIII. He says the successful ecosystem built by the top two vendors “…has relegated every other player lacking a strong ecosystem to the position of a price-taker. ”

The Northern Securities analyst says those expecting BB10 to vault RIM back into the rarefied air at the top of the space are likely to be disappointed, and RIM’s success will now be predicated on being relevant to the mid-market, which is extremely price sensitive. Kanade says the company is facing rapid margin compression that will continue even after the launch of BlackBerry 10. This means RIM’s cash position, once regarded as an important margin of safety in the transition period between the BlackBerry 7 and 10 platforms, is now a serious question mark.

_______________________

This story is brought to you by Serenic (TSXV:SER). Serenic’s cash position as of May 31st, 2012, $4.45-million, was greater than its market cap as of September 6th, which was $3.86-million. The company has zero long-term debt. Click here for more info.

_________________________

Kanade says he expects cash reserves to decrease materially at RIM. Margin erosion, he argues, combined with an inventory build up of BlackBerry 10 devices, will drive the company’s cash reserves to less than $600-million. He does not expect that the company can add revenues stream from things such as licensing its operating systems to other vendors until after the launch of BB10. The Samsung Galaxy S3

Kanade says RIM’s stock, which has fallen from more than $25 last October to recent lows under $7, is actually trading at a bit of a premium to its sum-of-the-parts value because of the potential for a buyout or major partnership. But he says, given the stance of management and key shareholders, that possibility should be regarded as remote, and will become more unlikely as the company’s fundamentals erode.

Research in Motion is scheduled to release its Q2 results on September 27, 2012, after market close. At press time, shares of the company on the TSX were down 3% to $7.02.

_________________

__________________

Nick Waddell

Founder of Cantech Letter

Cantech Letter founder and editor Nick Waddell has lived in five Canadian provinces and is proud of his country's often overlooked contributions to the world of science and technology. Waddell takes a regular shift on the Canadian media circuit, making appearances on CTV, CBC and BNN, and contributing to publications such as Canadian Business and Business Insider.

Related Posts

A headline yesterday in Canada was more akin to the tone of those we were used to seeing before the...

At a time when you’d think BlackBerry would be in full grip-and-grin sales mode, Thorsten Heins took a moment during...