Cargojet named a “Best Idea” at TD Cowen

In its Canada Best Ideas 2025 report, TD Cowen analyst Tim James maintained a “Buy” rating and C$160.00 target on Cargojet (Cargojet Stock Quote, Chart, News, Analysts, Financials TSXV:CJT), arguing the company’s fundamentals remain undervalued even amid trade-related uncertainty.

“Our $160.00 target price is based on a 9.0x EV/EBITDA multiple applied to Adjusted EBITDA for Q3/26–Q2/27 and net debt as at Q2/26,” James said. He added that current valuation multiples place Cargojet at its steepest discount to peers in more than a decade, providing room for re-rating as investor sentiment shifts.

The key risk identified is the elimination of U.S.-bound de minimis exemptions outside China, which took effect Aug. 29 after a similar China-only move in May. James estimated that only 5% to 10% of Cargojet’s total volume is exposed, and that a one-third decline of that slice is a reasonable assumption given prior experience.

“If the impact on Cargojet’s volume is greater than expected, it could negatively impact our target and forecasts,” he cautioned.

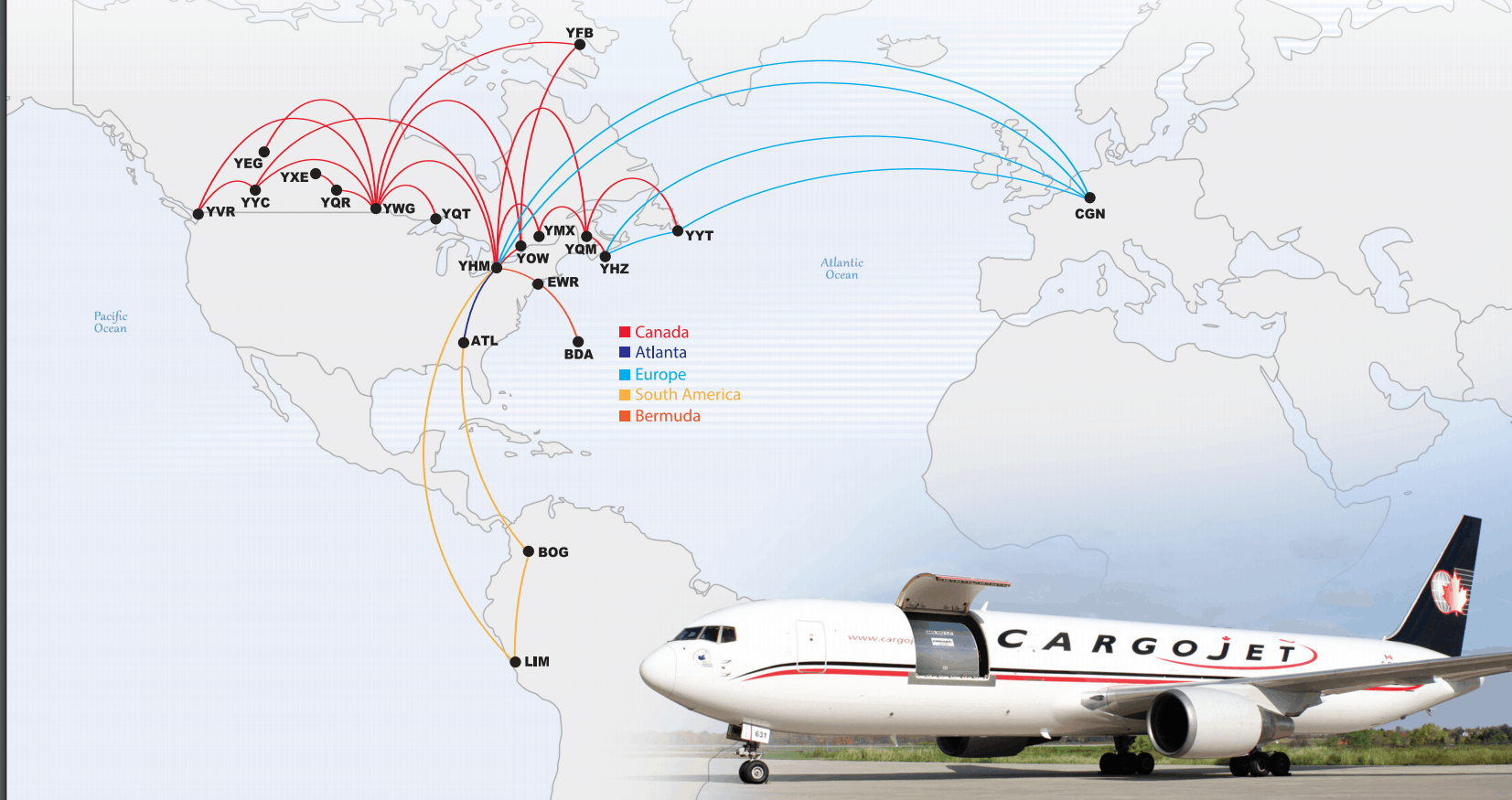

Founded in Canada, Cargojet operates overnight air cargo services with its own fleet and maintains long-term agreements with major global customers. Its contracts include minimum volume guarantees and price escalators, insulating a large portion of revenue from spot pricing. TD Cowen estimates roughly 90% of domestic revenue and 80% of ACMI revenue are protected under such terms, while about 30% of charter revenue is covered under minimum flight agreements.

James pointed to several strengths underpinning the stock, including Cargojet’s roughly 90% share of Canada’s domestic overnight air cargo market, high barriers to entry from ownership and operating regulations, and strong contract visibility. From 2021 to 2024, the company’s EBITDA grew at a 4% CAGR compared with flat growth for peers and modest global air cargo volume increases.

A recently announced 10-year agreement with DHL, replacing an earlier seven-year deal, was highlighted as a catalyst. TD Cowen estimates the new agreement could lift average annual revenue by about 20% versus the prior contract, though James said the full step-up is not guaranteed. Still, the contract was signed with DHL, already aware of the pending de minimis changes, which James views as further de-risking future earnings.

Scenario analysis indicates potential downside to about $105 in 12 months if trade risks materialize more sharply, but upside to more than $210 if fundamentals drive multiple expansion.

“We think trade-related risk to CJT volume is overly discounted in the current valuation and that positive business-specific developments are de-risking future upside,” James said.

He forecasts Adjusted EBITDA of C$319.2-million on revenue of C$993.5-million in fiscal 2025, rising to C$337.3-million on C$1.04-billion in 2026.

TD Cowen’s Canada Best Ideas 2025 highlights its highest-conviction Canadian picks across a coverage universe of nearly 1,300 companies, with more than 80 analysts contributing research.

-30-

Nick Waddell

Founder of Cantech Letter

Cantech Letter founder and editor Nick Waddell has lived in five Canadian provinces and is proud of his country's often overlooked contributions to the world of science and technology. Waddell takes a regular shift on the Canadian media circuit, making appearances on CTV, CBC and BNN, and contributing to publications such as Canadian Business and Business Insider.

Related Posts

Paradigm Capital analyst Razi Hasan says Cargojet (Cargojet Stock Quote, Chart, News, Analysts, Financials TSX:CJT) has managed well through a...

National Bank Financial analyst Cameron Doerksen says Cargojet’s (Cargojet Stock Quote, Chart, News, Analysts, Financials TSX:CJT) growth outlook remains broadly...