Is the shift toward programmatic CTV really inevitable?

We feel obligated to disclose that ChatGPT, the conventional wisdom machine, disagrees with our viewpoint in this article. By scouring the troves of Internet data (probably the best definition of consensus we have today), it has decided that programmatic advertising is highly suitable for the connected TV medium. We don’t agree. We make the case that a combination of factors, including privacy concerns, limited inventory supply, strong publisher power, a lack of standards and linear TV baggage will dampen the infiltration of open programmatic in CTV. We argue that CTV is where website development was in 2005. We didn’t have Squarespace, Wix or Shopify to help us build a web page in 10 minutes. We needed to rely on tech-enabled manage services hybrids to guide us on how to build a compelling website. We didn’t have the technical know-how, graphics, content or best practices. It is these types of vendors that will help brands navigate the CTV boon and win over the next three to five years.

So who are you going to trust? ChatGPT or this humble author?

The Easy Part: CTV is Big

We won’t spend a lot of time trying to convince you that connected TV is a big deal. That ship has sailed and we all know it’s a big deal. CTV video impressions now exceed mobile and PC for the first time.

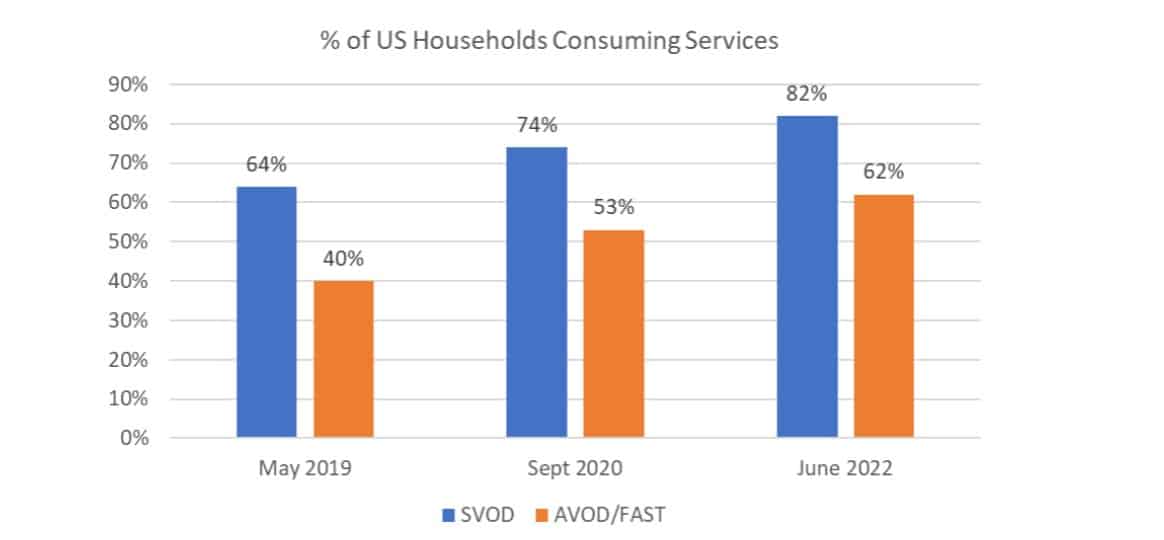

The next question is one of advertising. The growth of CTV viewership was driven by subscription-based premium services (SVOD) like Netlfix, Amazon Prime, HBO Max, Disney+, etc. SVOD now looks to be relatively mature with over 80% of US households now being subscribers of at least one premium service. The next big theme in CTV is going to be free and ad-supported models. Consumers have pushed back on the number of premium services they are willing to pay for and so many of the SVOD providers have launched ad-supported plans (AVOD). Peacock, Hulu and Paramount+ are active in AVOD but Netflix launching its ad-supported tier in November 2022 was a major industry shift lending further substance to this trend. AVOD allows consumers to pay lower subscription fees by watching ads.

This segment has about 28% market share within US households. Lastly, the number of free ad supported TV (FAST) channels has been ramping quickly, garnering about 24% market share in the US. There are over 1,500 FAST channels at last check with some of the largest being Pluto TV, Tubi, Crackle and Roku channel.

So how far have we come? CTV streaming is a big deal. With the saturation of SVOD and consumer pushback on pricing, the growth of AVOD and FAST is a logical step. The next question is, will the advertising dollars follow the eyeballs. History has shown that the answer tends to be yes whenever there is a gap between viewership and ad dollars.

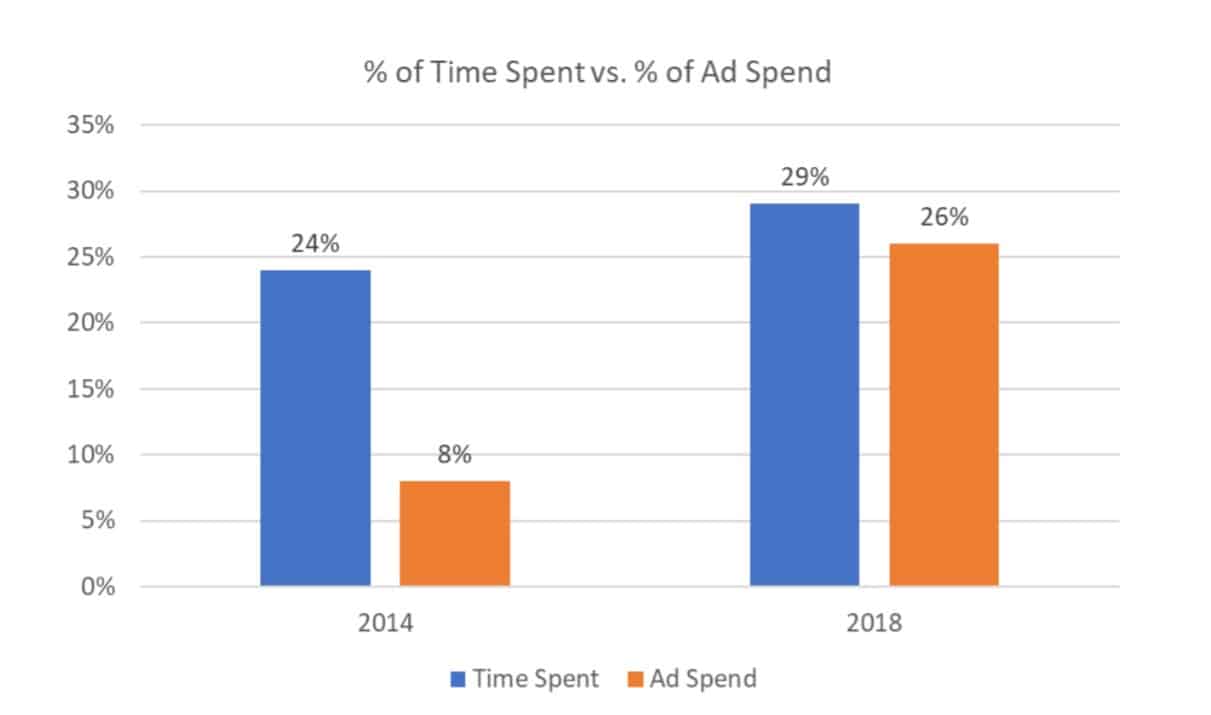

We always found value in the time spent vs. ad spend analysis presented by Kleiner Perkins throughout much of the last decade. For example, in 2014, the gap between time spent and ad spend for the US mobile industry was about 16%, according to Kleiner. By 2018, this gap had narrowed to 3% and today it is roughly zero. These arbitrage opportunities tend to resolve themselves sooner or later.

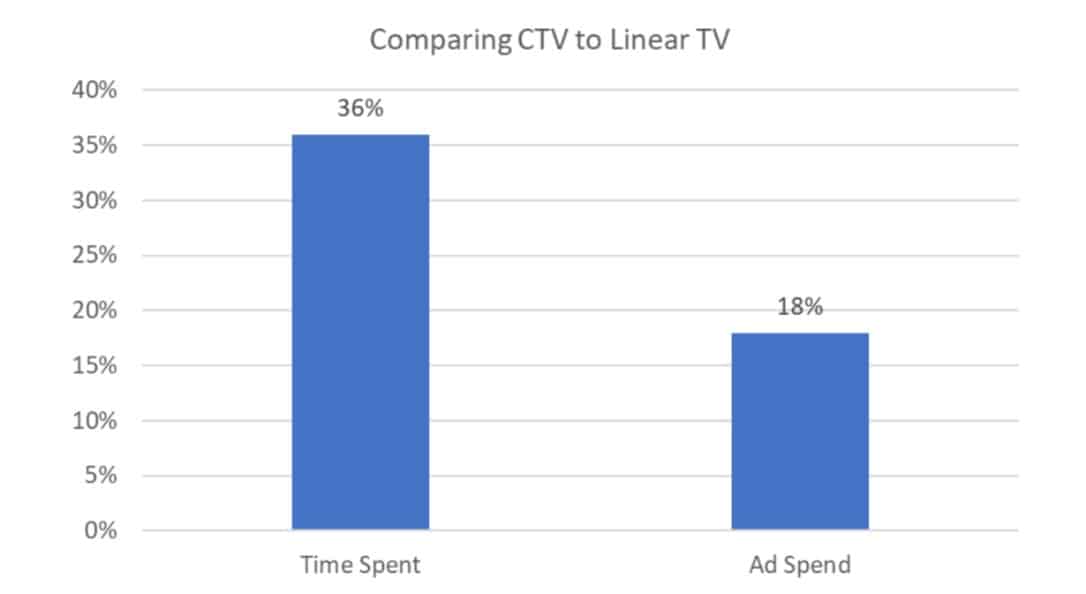

So what would similar data tell us today for the CTV market? As evident below, there is a major gap between CTV and linear TV. CTV has risen to taking 36% of the viewing time compared to linear TV and yet only 18% of the ad spend. Advertisers have already acknowledged this discrepancy and virtually all major TV advertisers are shifting some portion of their spend to CTV.

The Hard Part: Who Wins?

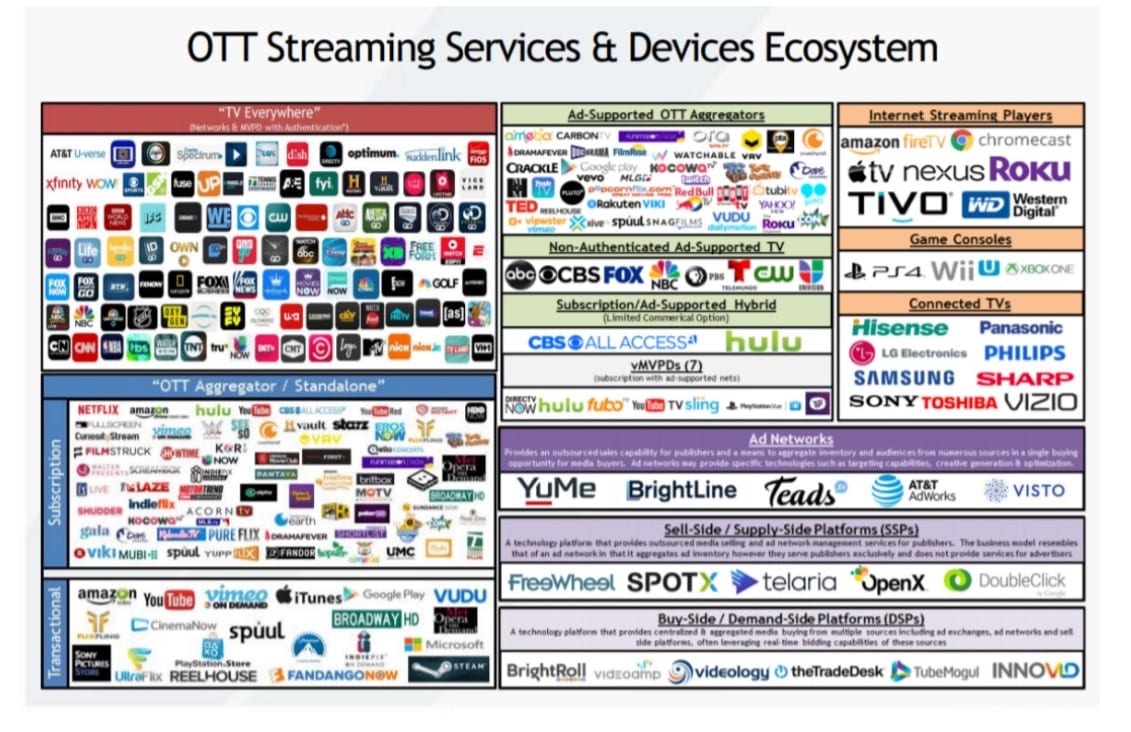

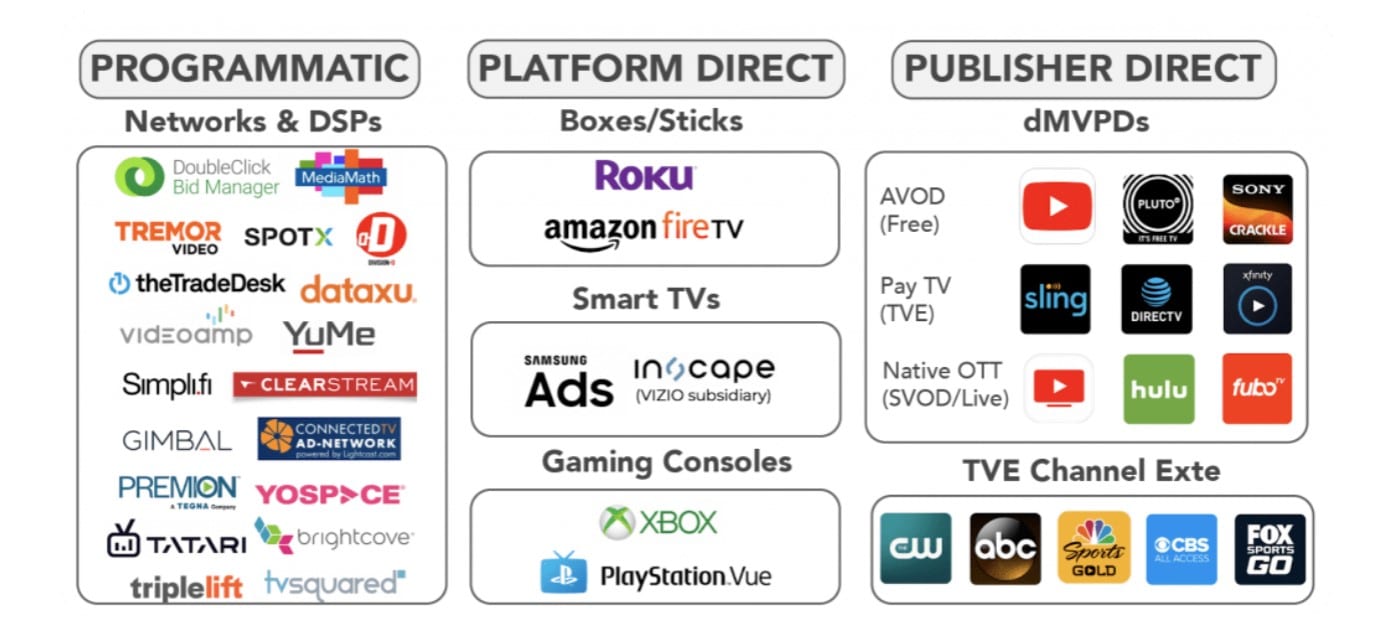

To summarize, macro trend number 1 is the growth of CTV. Macro trend number 2 is the shift toward ad supported content. The next big question is figuring out who wins. This section is a bit trickier. Massive growth trends tend to invite lots of new entrants, from the incumbents in adjacent industries to the startups. The figure below illustrates some of the complexity and key players in the market.

Let’s zoom down into just the advertising portion of the ecosystem. Cutting through the complexity, you’ll notice that the rules of engagement are broadly consistent with typical internet advertising. Advertisers can purchase inventory either direct or programmatic and if you’re going direct, you can

work with either the publisher (Netflix, Disney+) or the platform (Roku, Amazon FireTV).

Is CTV Ripe for Open Programmatic?

Now is when things get tricky. So far, we’ve told you that it’s 1997 and the Internet is going to be big. But the real question is, who wins. So let’s get into it.

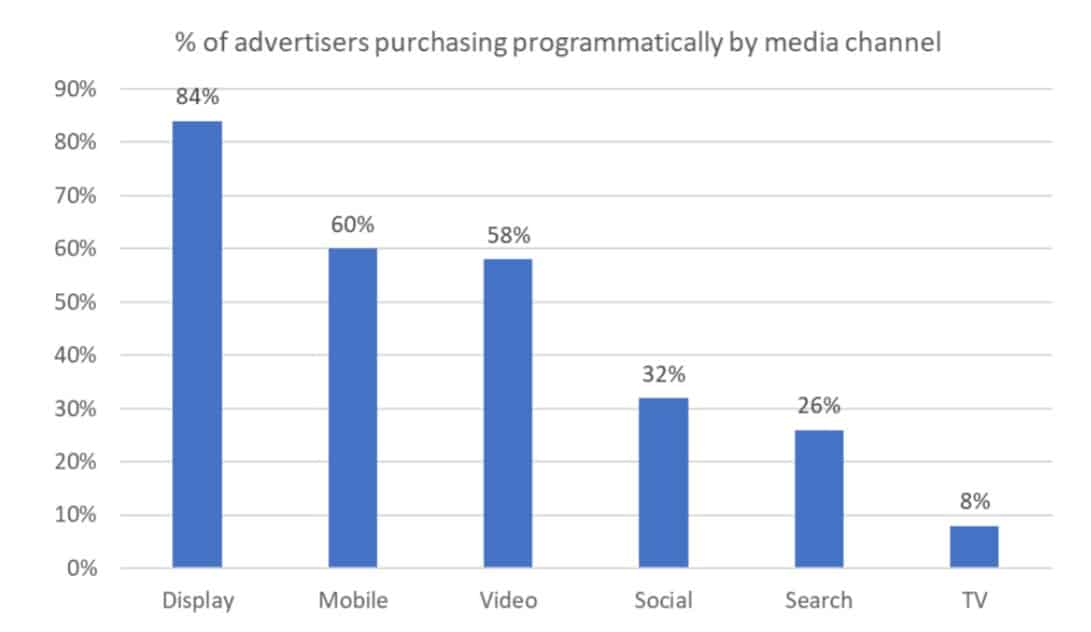

The first question in our mind is, how closely will the CTV ad market mimic the display or mobile markets. We’ve seen analysts argue that CTV advertising is just about to hit the inflection point in terms of viewership and market penetration, which will cause a massive swing toward programmatic advertising. Both the display and mobile markets experienced seismic shifts in programmatic market share, growing from sub 20% to over 70% programmatic in the span of 5 or so years. Should CTV follow the same curve? We don’t think so. We note that the programmatic market share is still very inconsistent by media channel. Although the data presented below is a few years old, the same premise holds. We believe there are structural reasons why display and mobile are almost fully penetrated with programmatic and social, search and TV are highly under-penetrated. We make this point to argue that blindly extrapolating the programmatic curve to CTV might not make the most sense.

Under what circumstances does open programmatic advertising thrive?

1. When privacy concerns are a non-factor. Programmatic and real-time-bidding (RTB) are very effective when apps track everything that you do without your knowledge. This has been major secular tailwind that has helped companies like Facebook, Snap and many DSPs grow unchecked for a decade. Now that privacy and data tracking have become major pain points for governments and consumers, many of these companies have seen market shares and valuations dwindle. The value proposition for programmatic has been eroded now that the cookie cheat code has been removed. The conclusion is that targeting needs to be done differently across the board and especially with CTV. Tradedesk is pushing UID2 as a potential solution but it’s still relatively early days with only 15% of the company’s third party data having UID2 tags associated with it.

2. When there is virtually unlimited supply of inventory. Display and mobile offer virtually unlimited inventory supply because every website, every search, every game and every app offer hundreds of potential impressions per visit per consumer.

3. When publisher fragmentation is high. Advertising relationships on the web used to be direct as well in the early stages of the Internet. When a few big websites dominated traffic, a large advertiser could secure high reach by negotiating direct relationships with the likes of AOL, ESPN or Yahoo. As millions of new websites emerged, it became impractical to negotiate direct deals and so programmatic became a much more efficient way to market across the web with scale.

4. When standards have emerged. Advertisers tend to prefer direct relationships with publishers when there is room to maneuver on the creative aspects of the ad. Ad duration, interactivity, full page takeovers and all sorts of other variability can be exploited to generate great ROI when direct relationships are secured. The problem is that these do not scale well. Display and mobile ads have been standardized by the publisher so that ads can all look the same and therefore fit within the algorithm parameters.

Now let’s apply these criteria to the major media channels above. Display and mobile fit all of the criteria and so their programmatic market share is very high. Why do Social and Search have much lower programmatic market share? Probably, because publishers are not fragmented and actually carry a lot of power. Google owns the Search market and has decided to monetize via its own proprietary CPC (cost per click) technology. Facebook and a few other major players dominate the Social market and they have built robust walled gardens to control access to their inventory. And why is TV so low on the programmatic scale? Because a few large networks own the inventory and supply is much more finite, especially for the coveted programming.

What about CTV? This is where we might differ from the consensus. We do not anticipate a smooth linear growth trajectory of open programmatic in the CTV market. Full disclosure: the conventional wisdom machine, ChatGPT, disagrees with us. Ask ChatGPT whether programmatic ads are highly suitable for CTV and you’ll get a resounding yes. Here’s why we disagree:

– Privacy is top of mind – a big shift away from traditional data tracking is taking place and CTV is not immune. The market will need to move toward first party and contextual data before programmatic can really take off in CTV

-Supply is limited – most CTV programming will serve about 4 to 6 minutes of ads per hour. Typical ads are 15 to 30 second spots and so this would translate into somewhere between 10-20 ads per hour. Watch a couple of hours of CTV and you might see 50 ads. Compare that to the number of ads you’ll be exposed to if you spend a few hours browsing, mobile gaming or on social media. A typical person is exposed to about 5,000 to 10,000 ads per day to give you some sense of magnitude.

-Publishers hold a lot of power – CTV streaming is dominated by a few big streamers (Netflix,Apple, Amazon, Disney, etc.) and a few big platforms (Roku, Amazon FireTV, etc.). Walled gardens dominate the CTV landscape. These big publishers are selling their prime inventory at $60+ CPMs, compared to more traditional Internet advertising at $5-15 CPMs.

-Standards have not yet emerged – yes, there are 15-30 second ad spots just like with traditional TV but there is also a lot of work being done on the dynamic and creative aspects of CTV advertising. Clickable ads or QR codes have been shown to dramatically improve engagement. Also, standards for data collection and sharing are slow to emerge because those big publishers listed above tend not to play nice in the sandbox. There is a good degree of rivalry among the leading players, which tends to lengthen of process of reaching some form of consensus.

There is one other factor that will disrupt the smooth transition toward open programmatic in CTV – the fact that most CTV budgets are being driven by a shift away from linear TV. Linear and CTV buying tends to be managed by the same team. The team that is driving the linear TV process will be much more

comfortable with the direct purchasing model rather than programmatic. The learning curve is steep with programmatic, which will also hamper the growth trajectory into CTV.

Implications for the Vendor Landscape

If we’re right that programmatic adoption will not be as rampant as quickly in CTV as it was in display and mobile, what does this mean for the vendor landscape? We believe that it means tech-enabled managed services will win out in the short to medium term. There was a time not too long ago when creating a website was the domain of the IT expert. Lengthy consultations would be required to figure out the design and implementation of a good website, not to

mention a lot of technical coding knowledge. Websites were custom built and very different from each other. Now, we’ve basically standardized them. I don’t need a software developer to build a website. I can use Squarespace or Wix or Shopify to build a page in about 10 minutes. CTV advertising is not at the Squarespace or Wix curve in the market. CTV advertising is where website development was in 2005. It’s at the tech-enabled managed services end of the spectrum. This means that self-serve DSPs who own the mobile and display markets will not conquer the CTV space anytime soon.

Here’s what we believe the top tier tech-enabled managed services company will offer to advertisers looking to profit from the CTV boon:

-Access to proprietary mid tail supply – the global brands will work directly with Netflix or Disney to ensure they have top tier inventory and they will pay handsomely for this privilege ($60-80 CPMs). However, what about the next 10-50 CTV channels? They don’t have the scale to work directly with advertisers. And we believe they will offer a better ROI because smaller channels likely have a more specific demographic, which the right brand can target for lower CPMs. The right managed services provider will establish relationships with CTV publishers numbered 10 to 50 so that they can offer a portfolio of unique audiences to brands.

-Contextual data – the right provider will use privacy-compliant data from multiple sources, including the publishers to offer better targeting capabilities to mid-tier brands that can not afford to enter into multi-million-dollar direct relationships with the top three publishers. Privacy concerns and Apple’s IDFA have made behavioral targeting much more difficult. Without opt-ins and stored cookies, advertisers will need to rely much more on context and first party data. What does this mean? It means that someone watching the Top Gun Maverick beach scene on a hot day might be more interested in a beer commercial than a hot soup commercial. And yes, the right provider will integrate real time weather reports into their contextual advertising.

-Creative ad design – the right provider will bring best practices to their brands. They will know that CTV ads do not need to mimic linear TV ads. There is a new world of engagement and interactivity available to CTV-focused brands. And consumers have so far responded very well to these ads with engagement rates that are 5x higher vs. similar ads in the mobile and PC side. The interactivity is generally built with QR codes or clickability. Other successful creatives have included more of a story design where the technology will know that you’ve seen the first version of the beer ad and will therefore show you the second version dynamically. A new consumer will not be shown the second ad until they have seen the first one. Finally, the right ad can be made to appear at the right time in the movie. The last thing I want to see while watching a gory horror movie is an ad about hot dogs or really any other food. Save those ads for when I’m watching Moneyball or Field of Dreams.

-Reporting translation – one of the biggest issues of walled gardens advertising is that everyone reports things differently and so getting a standard view can be very challenging. There is too much opacity in how publishers and platforms report their numbers and so developing an understanding whether your results on Roku were better than your results on FireTV, is challenging. This is where a knowledgeable managed services provider can make all the

difference.

-Helping smaller advertisers scale – the vast majority of CTV inventory is not available on open programmatic exchanges. As discussed, the industry isn’t there yet. Most inventory is available via private marketplace (PMP). This is a relatively exclusive VIP club, which doesn’t invite everyone to the game. The right provider will consolidate some portion of mid-sized buyers in order to give them sufficient scale to access these private auctions. Grouping 10 brands in order to achieve seven figure buying power will be an important value add.-

– Technical programmatic expertise – programmatic cannot be ignored. It is coming and will offer compelling ROI in the right niches. The right vendor will have the technical DSP, SSP and analytics capabilities to start helping brands migrate toward understanding where they should be working direct vs. programmatic to achieve wholistic business results.

In short, the right company at this time is a chameleon. It will help its marketing clients navigate this CTV juggernaut as a trusted advisor with amazing technical and creative capabilities. There is one company in our portfolio, which generally fits the bill on most of these criteria. Sabio, listed on the TSXV under the symbol “SBIO”, is a California-based AdTech company specializing in connected TV. They’ve managed to grow their CTV/OTT business over 140% in 2022 by focusing on providing great service to a market that isn’t yet ready to flip the switch to open exchange programmatic advertising. We expect that CTV advertising will remain a high-touch hybrid model for some time to come, which should benefit tech-enabled managed service companies like Sabio.

Conclusion

1. Connected TV is big and will get bigger, driven by free and ad-supported models.

2. There are structural reasons why open exchange programmatic will not infiltrate CTV as quickly as it did mobile and display.

3. We see a five-year window where hybrid managed services companies with great tech and white glove service will fill the needs of the CTV ad buyer.

Disclosure: Sabio is an annual sponsor of Cantech Letter

Dushan Batrovic

Writer

Dushan is an investor, founder, and former CEO and CFO of various technology companies. He is a Managing Director with Antera Inc., a venture capital and merchant banking firm focused on assisting early to mid-stage tech firms. He was previously on the Board of Directors for an Antera portfolio company and was a sell side equity research analyst and a VP at a private equity and venture capital fund. Dushan holds an MBA from the Rotman School of Management, University of Toronto. He also holds a Bachelor of Applied Science and Engineering at the University of Toronto and has earned his CPA designation.