The stock may be down over the past year but better-than-expected quarterly numbers have Beacon Securities analyst Ahmad Shaath staying bullish on Cargojet (Cargojet Stock Quote, Charts, News, Analysts, Financials TSX:CJT). Shaath devliered a report to clients on Thursday where he reiterated his “Buy” recommendation while lowering his target due to multiple contraction in the markets.

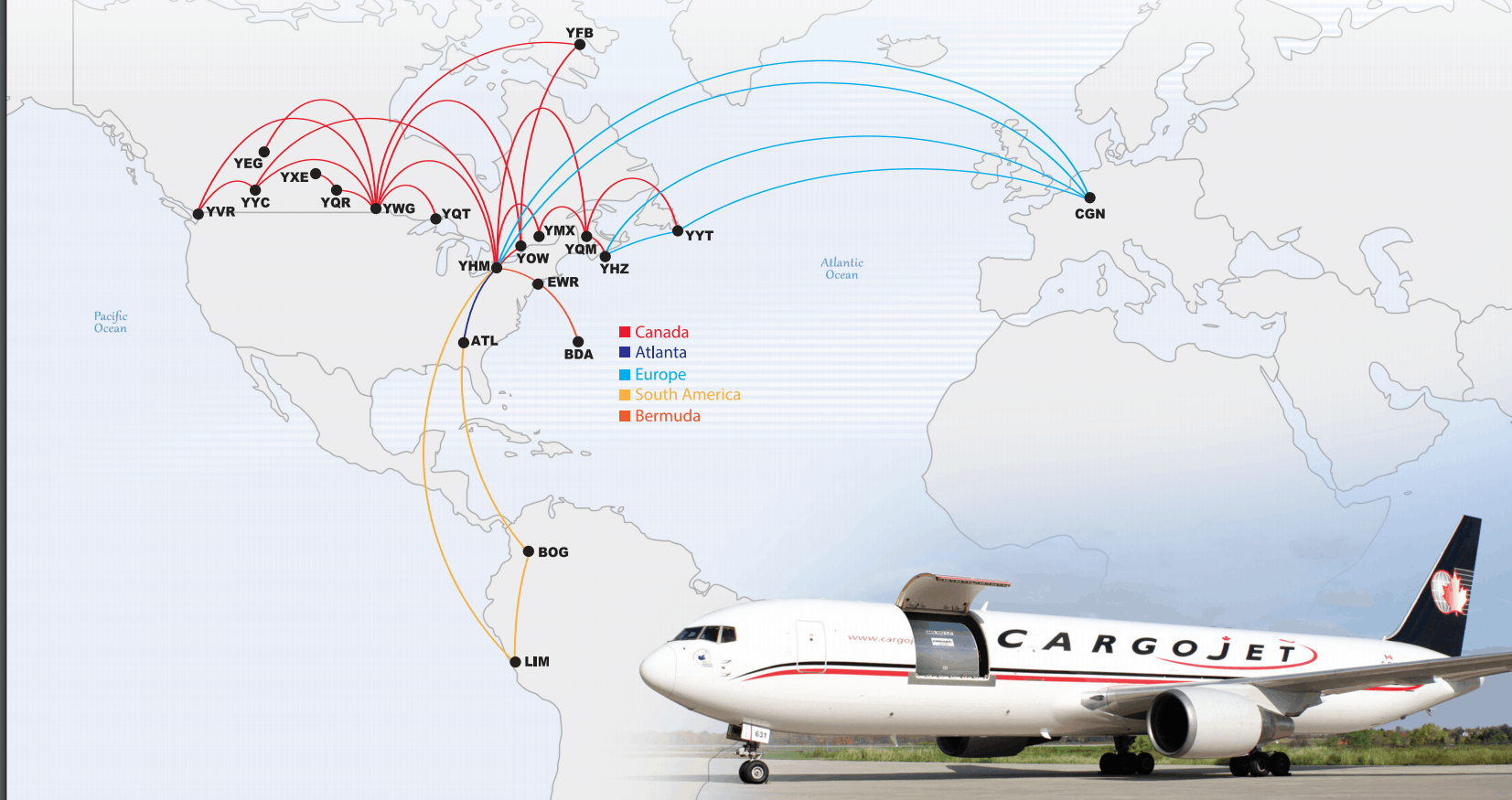

Cargojet, which in addition to its overnight cargo business across North America has an ACMI (aircraft, crew, maintenance and insurance) leasing business and a charter plane service, announced on Thursday its second quarter 2022 financials. The company reported total revenue of $246.6 million, up 43.3 per cent year-over-year, and adjusted EBITDA of $81.1 million, also up 20.3 per cent. By segment, Cargojet said its Domestic freight revenue was up 15.0 per cent, ACMI was up 62.4 per cent and All-in Charters was up 23.2 per cent.

President and CEO Ajay Virmani said CJT is feeling the weight of global forces such as inflation, fuel prices and geopolitical uncertainties and so management is aiming to balance investing in growth and maintaining a strong balance sheet over upcoming quarters.

“Unpredictability of belly space was the reason Cargojet was born over 20 years ago. From the first day of our existence, we have focused on doing just one thing – flying cargo. That’s our sole purpose and mission. We have built a brand that is trusted by our customers to keep its promises and the recent macro events have further strengthened our resolve to stay focused on serving our customers,” said Virmani in a press release.

Further to the macro environment, Cargojet said passenger airlines are also facing “extremely difficult” operating conditions, which in turn is impacting air cargo supply chains.

“The impact of rapidly shifting schedules and poor on-time performance of passenger airlines has further restricted the ability of cargo shippers to utilize belly space. This, combined with ongoing supply chain challenges, continues to provide opportunities for Cargojet to capture unmet demand in the medium term,” CJT’s press release said.

Nevertheless, Shaath said the quarter was a beat, with the $247 million topline coming in ahead of his estimate at $220 million and the consensus $231 million. CJT’s Domestic segment’s 15.0 per cent revenue growth was also above Shaath’s estimate at 5.9 per cent, while ACMI revenues of $60 million were also better than the analyst’s call for $52 million. The latter improvement was mainly due to DHL redirecting a route from Europe to China, Shaath pointed out.

“The company continues to see strength in demand for dedicated cargo, providing a solid foundation for continued growth in ACMI, offset by a moderate slowdown in ecommerce demand that is impacting its domestic network,” Shaath wrote.

Earnings were also a beat at $81 million EBITDA compared to Shaath’s $80 million estimate and the Street’s $79 million.

Shaath noted that on the earnings call management spoke of a slowdown in e-commerce trends, although the expectation still was for double-digit growth in the domestic network for the full 2022 year.

“The company is seeing a shift in mix in consumer spending, away from luxury items and towards daily basic needs. We view it as a solidification of the secular growth trend in e-commerce and a reflection of Canada’s lag versus G7 counterparts in e-commerce penetration,” Shaath wrote.

With the new results, Shaath has tweaked his forecast and is now calling for full 2022 revenue and EBITDA of $1.029 billion and $355.0 million, respectively, and for 2023 revenue and EBITDA of $1.046 billion and $384.0 million, respectively. Shaath has CJT’s EV/Sales going from 3.9x in 2021 to 2.8x in 2022 to 2.8x in 2023 and the EV/EBITDA multiple going from 10.0x in 2021 to 8.2x in 2022 and to 7.6x in 2023. The company’s P/E is set to go from 22.4x in 2021 to 16.1x in 2022 to 13.7x in 2023.

“While the stock has ben pressured due to negative headlines regarding general macroeconomic trends, and more specifically e-commerce growth trends, we believe positive catalysts will continue to come from the ACMI business line (a ~70 per cent EBITDA margin business),” Shaath wrote.

Shaath has moved his target from $275.00 to $220.00, which is based on an EV/EBITDA multiple of 12.0x versus 15.0x prior.

“At current valuation of just 7.6x FY23E EBITDA with two-year revenue and EBITDA CAGR of 17 per cent and 14 per cent, respectively, CJT shares have never represented a better risk-reward trade. We maintain our BUY recommendation,” Shaath wrote.

About The Author /

Jayson is a writer, researcher and educator with a PhD in political philosophy from the University of Ottawa. His interests range from bioethics and innovations in the health sciences to governance, social justice and the history of ideas.

RELATED POSTS

Share

Share Tweet

Tweet Share

ShareTRENDING

All Trending →

TTNM keeps “Buy” rating at Haywood

March 20, 2024

NEO stock has price target chopped at Paradigm

March 18, 2024

Groupon’s turnaround is accelerating, Roth says

March 18, 2024

Comment