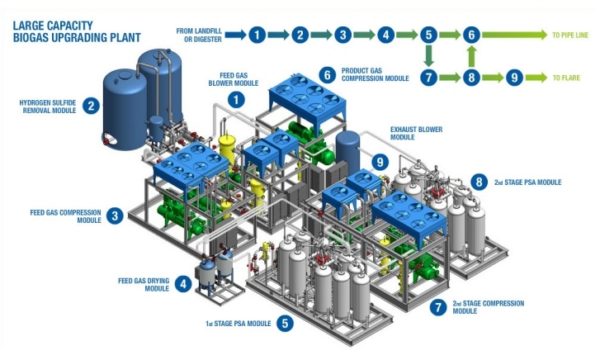

Xebec Adsorption has huge potential, M Partners says

Following the company’s first quarter results, M Partners analyst Andrew Hood is maintaining his “Buy” rating on Xebec Adsorption (Xebec Adsorption Stock Quote, Chart TSXV:XBC).

This morning, Xebec reported its Q1, 2019 results. The company earned $400,000 on revenue of $9.8-million, a topline that was up 206 per cent over the same period last year.

“The renewable gas industry is finally making headway, CEO Kurt Sorschak said. “The recent announcement of UPS to source 170 Million Gallon Equivalents of RNG over a seven-year period from Clean Energy Fuels Corp., is the largest ever purchase of RNG in U.S. history. This will reduce as much as 1 million metric tons of GHG emissions over the life of the agreement. It is equivalent to planting 17,000,000 trees, removing 228,000 cars off the road, or recycling 374,000 tons of waste that would otherwise be sent to the landfill. UPS drives more than 6,100 CNG and LNG vehicles which can be powered by RNG, allowing these staggering reductions in lifecycle greenhouse gas emissions when compared to conventional diesel. Heavy duty transport and public transit vehicles are ideal for RNG as a transport fuel. Environmental benefits are significant, and the technology is fully commercial and readily available, contrary to either fuel cell or battery technology which has not yet reached the same stage of development as RNG for heavy duty applications. RNG is a unique fuel derived from organic waste materials that links the circular economy – from energy production in the form of zero-carbon transport fuels benefiting the environment, through other participants in the waste generation and processing industries like farmers, food processors, municipalities, waste companies, and others. Xebec looks forward to playing a leading role in the future development of this emerging industry.”

Hood says Xebec’s revenue figure fell below the $12.3-million he had expected, though it beat the street consensus of $9.2-million. But the analyst says a number of factors, including a growing backlog, make him optimistic.

“Following our call with CEO Kurt Sorschak, we remain optimistic about Xebec’s opportunity in 2019 and beyond,” Hood says. “At the time of our last update, Xebec had indicated it had $540M in quotes out globally. In just a couple months, this figure has expanded to $760M. Management anticipates capturing $150-200M of these quotes as orders over the next 24-36 months. Even for its current order backlog of $71M, Xebec should be able to recognize $35-40M in revenues in 2019. We also highlight the potential for significant contract wins beyond our expectations over the next couple years. For example, Spain is in the process of crafting its renewable natural gas policies, and Xebec is aiming to serve the market once these policies are in place. XBC also continues to build out its new Build, Own, Operate segment, which has potential to become its biggest revenue driver and provide recurring revenues in the long run. Earlier this month, the Board of Directors approved a strategy to expand this segment and engage with a larger number of potential partners to explore opportunities in Canada and California.”

In a research update to clients today, Hood maintained his “Buy” rating and one-year price target of $2.20 on Xebec, implying a return of 40 per cent at the time of publication.

The analyst thinks XBC will post EBITDA of $6.5-million on revenue of $48.0-million in fiscal 2019.

“For the purposes of our target price, our valuation is based on a short-term forecast – longer term we believe Xebec will only continue to generate value for shareholders,” the analyst adds. “Since our forecast is focused on the short term, we do not factor in any contributions from the BOO or Power-to-Gas segments, which could ultimately contribute half of Xebec’s revenues in the long-term. We also note that even our short-term forecast would need to be revised in the event that Xebec signs even one landfill order in the U.S. A single order could add $15-30M in revenues and

$3.7-7.5M in EBITDA on top of our forecast.”

Nick Waddell

Founder of Cantech Letter

Cantech Letter founder and editor Nick Waddell has lived in five Canadian provinces and is proud of his country's often overlooked contributions to the world of science and technology. Waddell takes a regular shift on the Canadian media circuit, making appearances on CTV, CBC and BNN, and contributing to publications such as Canadian Business and Business Insider.

Related Posts

The stock has been beaten up pretty good over the past year, but now’s the time for investors to be...