Buy Baylin for exposure to antenna market growth in 2019, Paradigm says

Following the report of its 2018 results, Baylin Technologies (Baylin Technologies Stock Quote, Chart TSX:BYL) is set up for a prosperous 2019, Paradigm Capital analyst Kevin Krishnaratne says.

Following the report of its 2018 results, Baylin Technologies (Baylin Technologies Stock Quote, Chart TSX:BYL) is set up for a prosperous 2019, Paradigm Capital analyst Kevin Krishnaratne says.

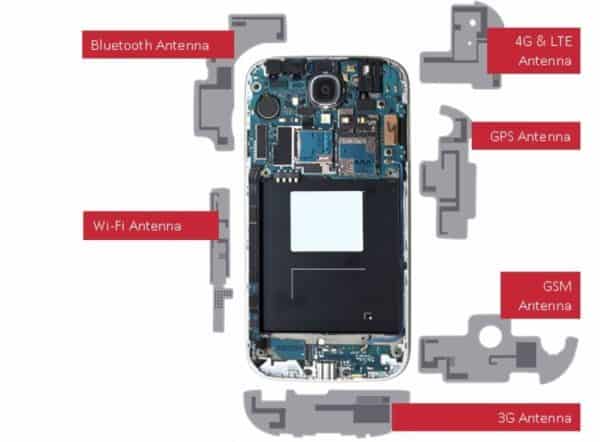

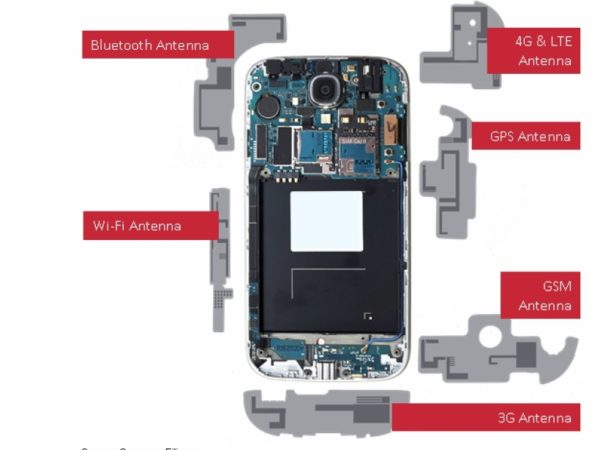

On Wednesday, Baylin reported its Q4 and fiscal 2019 results. In the fourth quarter, the company posted Adjusted EBITDA of $3.9-million on revenue of $36.0-million, a topline that was up 47 per cent over the same period a year prior.

“We are very pleased with the company’s progress in 2018,” CEO Randy Dewey said. “The company’s revenue base has continued to diversify with growth in the embedded antenna and wireless infrastructure groups and through the acquisitions of Advantech Wireless and Alga Microwave.”

Krishnaratne says industry trends are putting the wind at Baylin’s back.

“BYL reported Q4 results that showed revenue growth of 47.9% y/y, driven by gains in wireless infrastructure products that are seeing success owing to the current 4G carrier densification capex cycle, which is still in its early days, in addition to the inclusion of M&A completed in 2018 (Advantech and Alga),” he says. “We look forward to 2019 trends which should continue to benefit from 4G densification and initial 5G rollouts, though the latter deployment will become much more meaningful in 2020 and beyond.”

In a research update to clients today, Krishnaratne maintained his “Buy” rating and one-year price target of $5.75 on Bayline, implying a return of 50 per cent at the time of publication.

The analyst thinks BYL will post EBITDA of $22.9-million on revenue of $165.5-million in fiscal 2019. He expects those numbers will improve to EBITDA of $28.2-million on a topline of $180.3-million the following year.

“We arrive at our C$5.75 target using a 11x EV/EBITDA 2019e multiple. Our target also reflects a ~9.0x EV/EBITDA multiple on 2020 estimates which is in line with the peer group average currently trading at 8.9x,” he adds. “We like the stock for its leverage to carrier densification plans in 4G, which should continue for several years, and for its potential to be a key supplier into the 5G capex upgrade cycle, while strength in carrier infrastructure sales alongside M&A into new markets continues to diversify the business and lower its reliance on Samsung in Mobile.”

Nick Waddell

Founder of Cantech Letter

Cantech Letter founder and editor Nick Waddell has lived in five Canadian provinces and is proud of his country's often overlooked contributions to the world of science and technology. Waddell takes a regular shift on the Canadian media circuit, making appearances on CTV, CBC and BNN, and contributing to publications such as Canadian Business and Business Insider.

Related Posts

Baylin Technologies (Baylin Technologies Stock Quote, Chart, News, Analysts, Financials TSX:BYL) CEO Leighton Carroll says the company is emerging from...

Paradigm Capital analyst Daniel Rosenberg has maintained a “Speculative Buy” rating on Baylin Technologies (Baylin Technologies Stock Quote, Chart, News,...