Shopify (Quote, Chart TSX, NYSE:SHOP) has been one of the notable high-fliers in the Canadian tech revival of the past few years. But does that mean that current investors have missed the boat on the stock’s upside? Is the Shopify stock forecast less rosy than its past?

Not necessarily, says National Bank Financial analyst Richard Tse, who says compared to other high growth tech names Shopify is more reasonably priced than you might expect.

Richard Tse’s Shopify Stock Forecast

“When it comes to our high growth names, we’re often asked whether the valuations that come with them are justified,” the analyst explained in a note to clients today. “On that question, we think we covered it in our recent implied growth analysis titled “Revisiting Valuation to Growth – Long Term”. The conclusion of that note was that we think valuations are justified provided the long-term growth outlook for the respective names stay the course to our expectations. In this note, we look to another fundamental measure for one of our pricier names that has had some controversy over the past year – Shopify.”

The National Bank Financial analyst says in this extended bull market, high valuations are being rewarded to high growth tech names that could be described as SHOP’s peers, such as ServiceNow (Quote, Chart NYSE:NOW), ETSY (Quote, Chart Nasdaq:ETSY), and Salesforce (Quote, Chart NYSE:CRM).

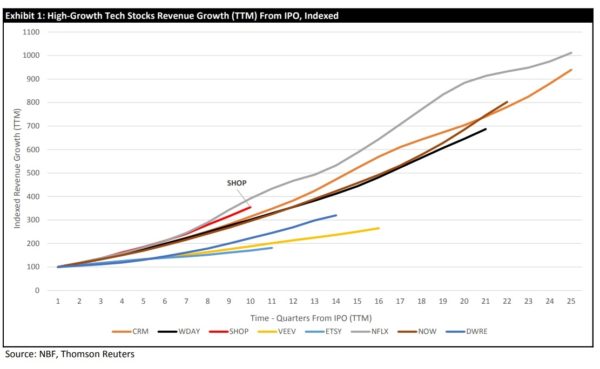

“The question we wanted to figure out is how Shopify’s growth rate is tracking relative to a group of high growth Tech names with similar attributes in an effort to gather another datapoint to determine whether Shopify’s relative valuation makes sense based on its financial performance and outlook,” Tse says. “We’re not saying this is the only measure we use to evaluate our names, but we think it’s certainly one to assess Shopify relative to other growth peers. To our surprise, Shopify is tracking towards the top-end of the peer group from a growth perspective when we compare it to other names at the same point in their growth timeline. Bottom line, given our growth outlook, it suggests the stock still has a long runway in front of it.”

Tse performed a comparable analysis of a group of eight successful high-growth names in their first 25 quarters from their respective IPO dates. He notes that Shopify is just three years in but says it will surprise some to find that the company’s base quarterly revenue compares favourably to household names such as Netflix (Quote, Chart Nasdaq:NFLX) and Veeva Systems (Quote, Chart NYSE:VEEV). Tse points out that SHOP’s base is around $45-million, compared to about $20-million for Netflix at the same time, so the company isn’t simply benefiting from a small base.

“Bottom line,” Tse says, “we continue to believe Shopify is early in a rapidly growing e-Commerce market. Like other disruptive leaders, we believe the upside in the stock comes from the underlying fundamental growth as we look beyond the short term. We reiterate our Outperform and US$180 target price based on our DCF. Our target implies EV/sales of 11.7x F19E (unchanged).”

About The Author /

Cantech Letter founder and editor Nick Waddell has lived in five Canadian provinces and is proud of his country's often overlooked contributions to the world of science and technology. Waddell takes a regular shift on the Canadian media circuit, making appearances on CTV, CBC and BNN, and contributing to publications such as Canadian Business and Business Insider.

Leave a Reply

You must be logged in to post a comment.

RELATED POSTS

Share

Share Tweet

Tweet Share

ShareTRENDING

All Trending →

TTNM keeps “Buy” rating at Haywood

March 20, 2024

NEO stock has price target chopped at Paradigm

March 18, 2024

Groupon’s turnaround is accelerating, Roth says

March 18, 2024

Comment