It’s much too early to tell if ProMetic Life Sciences’ (ProMetic Life Sciences Stock Quote, Chart, News: TSX:PLI) PBI-4050 drug candidate is going to be a blockbuster or not, but Echelon Wealth Partners analyst Doug Loe says all signs so far have been positive ones.

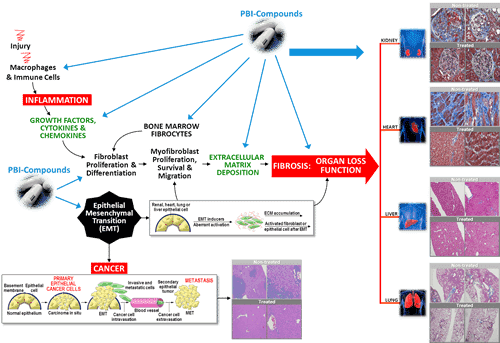

Yesterday, ProMetic reported that the PBI-4050 phase 2 clinical trial in patients with metabolic syndrome and Type 2 diabetes has been completed and has met its primary and secondary end points. The study, says the company, was meant to evaluate the effect of PBI-4050 on metabolic syndrome parameters and on pro-inflammatory/fibrotic and diabetic biomarkers in blood and urine, as well as test its to safety and tolerability.

“We are pleased to see that PBI-4050 continues to deliver the same solid results in patients with metabolic syndrome and Type 2 diabetes, but what is perhaps even more interesting is the meaningful reduction in biomarkers which when elevated are associated with cardiovascular and kidney complications,” said CEO Pierre Laurin. “This provides us with very valuable confirmation of efficacy in important parameters ahead of our upcoming placebo-controlled clinical trials.”

Loe says it is important not to over-interpret interim early stage clinical data, but says PBI-4050 has performed “about as well as it can” in all clinical contexts for which data are available. The analyst today maintained his “Buy” rating and one-year price target of $4.00 on ProMetic, implying a return of 24.6 per cent at the time of publication.

“We believe our existing financial forecast and valuation adequately reflect ProMetic’s consolidated pipeline development risk, a pipeline that includes not just flagship small-molecule drug PBI-4050, but also a suite of affinity-purified high-purity, high-activity plasma products that include Phase III stage plasminogen and IVIG currently, but down the road should also include alpha-1-antitrypsin and C1 esterase inhibitor and multiple other plasma-derived biologic therapies that are already commercialized by peers like CSL, Baxter and Grifols,” says the analyst.

Loe believes ProMetic will post negative EBITDA of $56.3-million on revenue of $32.2-million in fiscal 2016. He expects the company’s EBITDA loss will grow to $63.6-million on a topline of $35.1-million the following year.

About The Author /

Cantech Letter founder and editor Nick Waddell has lived in five Canadian provinces and is proud of his country's often overlooked contributions to the world of science and technology. Waddell takes a regular shift on the Canadian media circuit, making appearances on CTV, CBC and BNN, and contributing to publications such as Canadian Business and Business Insider.

Leave a Reply

You must be logged in to post a comment.

RELATED POSTS

Share

Share Tweet

Tweet Share

ShareTRENDING

All Trending →

TTNM keeps “Buy” rating at Haywood

March 20, 2024

NEO stock has price target chopped at Paradigm

March 18, 2024

Groupon’s turnaround is accelerating, Roth says

March 18, 2024

Comment